Dude, Just “Uber” Across the Ocean

Heidmar Maritime Holdings (HMR) is a commercial and technical management company, operates tanker and dry-bulk vessel pools worldwide.

Last three quarters showed triple digit growth and gross margins consistently >55%

Valuations

| Ratio | Value |

|---|---|

| Market Cap | ~$93M |

| Price / Sales | ~1.7x |

| Price / Book | ~8.7x |

| Enterprise Value | ~$74M |

| EV / Revenue | ~1.3x |

Q1 2026 performance witnessing over 200% year-over-year revenue growth.

CEO Pankaj Khanna explained that the growth was driven by both expanded vessel management and record-high shipping rates, particularly in the VLCC and Suezmax segments, with rates reaching $200,000-$700,000 per day.

Future Growth (Interview)

The existing revenue came from two primary sources. The first was Heidmar’s fee-based commercial and technical management activities. The second was proprietary vessel trading. During the quarter, the company operated eight to nine vessels in proprietary trading while also expanding its managed fleet.

Mr. Khanna recently in an interview has pointed out that tanker market strength was not solely a result of geopolitical conflict. He noted that tanker rates were already at historically high levels before the latest disruptions. “VLCCs were making over $200,000 per day. Aframaxes and Suezmaxes were in the $100,000-$200,000 per day range,”. While war in the Middle East has pushed rates higher, the results of this will show itself in the next quarters earnings.

He expressed confidence in continued growth through Q2 2026, including expansion in technical management and additional commercial mandates, while noting that recent stock price gains present a buying opportunity for long-term investors

They earn commissions on gross voyage revenues regardless of vessel ownership. This model achieved its first GAAP-profitable quarter in Q1 2026, outperforming consensus estimates.

Shipping differently

Heidmar largely does not own the ships.

Instead, it helps ship owners find cargo, optimize routes, manage commercial operations, and maximize earnings.

The company commercially manages a fleet of over 50 vessels — including VLCCs, Suezmax, Aframax/LR2, and MR product tankers — however, they also are in the other marine-related areas as well. Through its proprietary pool management platform, while also offering technical management, ship sale and purchase advisory, chartering services, and asset management.

Heidmar further differentiates itself through eFleetWatch, a proprietary digital platform designed to provide vessel owners, port agents, and brokers with real-time tools to monitor, track, and manage vessels, reinforcing its position as the original commercial pool manager in the tanker space

As a result, Heidmar runs an asset-light business model, with no debt or shipping assets. This is all being done with self-funding operations, too.

Analysts forecast EPS growth of 78.1% per annum and annual earnings growth of 77.6%, significantly outpacing both the US market and the oil and gas sector.

Missed the Boat?

Many company owners who had chartered vessels on fixed contracts missed the recent spike in spot market earnings. As these contracts come to completion they may now be seeking spot contracts and with this, commercial management support.

If you’re bullish shipping, there’s a reason to look into this company

Example: A tanker owner owns a $60-$120 million vessel.That owner needs cargo contracts, charterers, brokers, port coordination, scheduling, market intelligence, and revenue optimization. Heidmar provides those services for a fee.

If Heidmar eventually:

- licenses eFleetWatch to third-party owners,

- charges subscription fees,

- expands it into a maritime operating system,

Then the market could start valuing part of Heidmar like a maritime software company rather than purely a shipping services company.

Vote of Confidence So Far

The strongest external validation may be the continued relationship with major owners, especially entities tied to Evangelos Marinakis’s shipping group.

Roughly half of Heidmar’s managed fleet comes from Capital Maritime-affiliated vessels. The risk is concentration. But the flip side is that a sophisticated shipping owner has continued to entrust a large number of vessels to Heidmar.

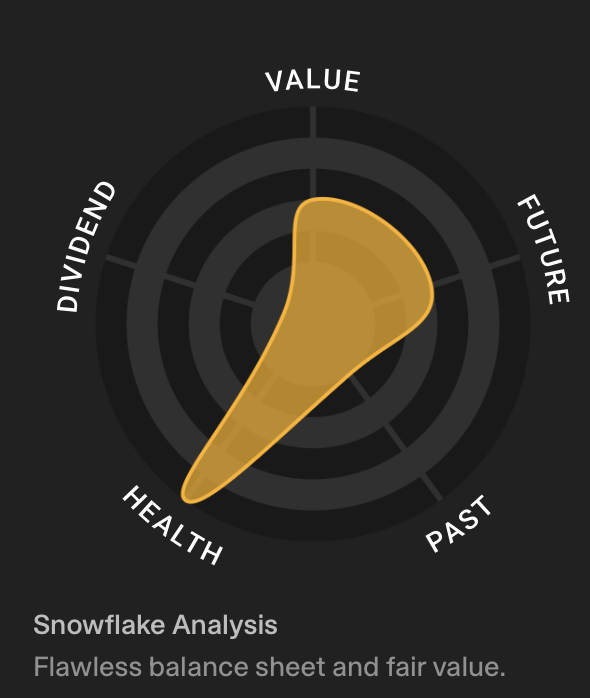

Balance Sheet

| Metric | FY2025 |

|---|---|

| Cash & Equivalents | $18.65M |

| Total Current Assets | $26.44M |

| Total Assets | $71.20M |

| Total Current Liabilities | $4.17M |

| Total Liabilities | $4.17M |

| Shareholders’ Equity | $10.71M |

| Net Cash | $27.6M |

| Total Debt | $0 |

| Book Value | $10.71M |

| Book Value / Share | $0.18 |

Cash reserves have grown to $27.6 million with zero debt, reflecting an autofinanced model where operational cash flow is now sufficient to support growth without relying on external capital. CEO Pankaj Khanna, who holds a significant ~45% stake, continues to buy on the open market, actively compressing the limited float.

Income Statement

| Metric | FY2025 |

|---|---|

| Revenue | $55.85M |

| Revenue Growth | +92.9% |

| Gross Profit | $14.30M |

| Gross Margin | 25.8% |

| EBITDA | -$4.80M |

| EBITDA Margin | -8.6% |

| EBIT | -$4.88M |

| Operating Margin | -8.7% |

| Net Income | -$8.64M |

| Net Margin | -15.5% |

| EPS (Diluted) | -$0.39 |

| Free Cash Flow | $10.68M |

| FCF Margin | 19.1% |

We're looking at definitely a growth-styled play

Problems with Trading (?)

Algorithmic price models forecast HMR falling to $0.78 by end of 2026, a 50% decline from current levels, citing extremely high volatility of 24.85% and a Fear & Greed Index reading of 39. The stock’s negative P/E ratio of -2.39 and history of trading far below analyst targets suggest the market is pricing in substantial execution and liquidity risk.

Concerns Worth Mentioning

Personally, I question whether this company’s growth proposition is worth the extra margin that we can simply buy with shipping companies now, of whom, are already positioned with huge amounts of cash for dividends. Buying this we’d have to do so understanding that we’re playing a growth company, instead!

One concern repeatedly raised by investors is that a meaningful portion of Heidmar’s managed fleet and revenue is tied to a relatively small number of customers. If a major customer moved vessels elsewhere or reduced business with Heidmar, the impact on revenue could be substantial. Of course, this can change for the upside, too.

While it seems to be cleared now, there was also the concern regarding nasdaq compliance regarding their share price–which is never a great sign.

Another point that I’ve already mentioned is that the CEO holding 45% of the company. This is more noteworthy given that the market cap is remaining somewhat small and the previous CFO recently walking, I’m skeptical that this company is only growing impressively (from a lower base) just to be dumped tremendously by management [when shipping falls into another cyclical bottom]. This is especially compounded by the fact that trading volume isn’t the highest.

Speaking about the CEO, Pankaj Khanna held senior roles at companies such as DryShips Inc. and Ocean Rig UDW Inc.

DryShips became infamous during the 2010s for:

- Poor outcomes for many minority shareholders.

- Massive shareholder dilution.

- Complex related-party transactions.

Lastly, it’s worth noting that they’ve been only profitable for 3 out of the last 10 years. This is not a deal breaker, but just a reminder as to their stage.

Closing

My recommendation? Watch this stock carefully–if they’re able to onboard more and more of the fewer and fewer shipping companies onto their platform and continue to grow, then it could be a very interesting moat they offer. For now, some of their margins are attractive, they have no debt, some established ships utilizing their management services and I believe they’re in the right sector for the near-term future.

On the other hand, there are some reasons to be concerned given the negative net income, the management shuffles, concentration risk, Nasdaq compliance talks, business model uncertainty and potential for heavy insider selling to rock the share price.

I normally start writing about stocks with the idea that I’m going to recommend a Buy, even within the context of the world falling to pieces–however if you currently own this I think this squarely fits the HOLD category and if you do not, it feels like you should be HOLD’ing off for now.

If you need any of the following, please email me with the subject “Serious Help”.