🚨Investment Powerplay🚨 Going International

Norway has been a jurisdiction that despite their increasing crime problems in Oslo and Bergen, their high taxation (+ stupid wealth taxes) and complete adoption of the climate scams and Muslim immigration, have a lot of attractive value stocks on their exchange. Norway has done extremely well with energy exports since Europe forced themselves to turn to their Northern neighbour (click here to see Norway’s budget surplus). I’ve recently said that the Nordic countries will fair the best in Europe in the future for a number of reasons.

I like foreign jurisdictions because there’s less big money headed there (less competition) and they tend to be more conservative with their balance sheets because Uncle Sam’s ATM isn’t there. The culture may be more geared towards returning dividends to shareholders as opposed to growth promises, too. It may be boring, but if someone doesn’t need to watch their Robinhood account every hour, this is a unique position.

Not a Shit Stock, a Fertilizer one

Yara International ASA is a Norwegian chemical company (YAR.OL). They specialize in global crop nutrition and industrial solutions company founded in 1905 and headquartered in Oslo, Norway, with operations in over 60 countries and approximately 16,600 full-time employees. The company produces, distributes, and sells a comprehensive range of nitrogen-based mineral fertilizers — including urea, calcium ammonium nitrate, and ammonium sulfate — as well as compound and specialty fertilizers containing nitrogen, phosphorus, and potassium, marketed under brands such as YaraBela, YaraLiva, YaraMila, and YaraVita. Yara also provides digital farming tools and precision agriculture solutions, including crop monitoring apps, N-Sensor technology, and fertigation services

| Metric | Latest Range |

|---|---|

| P/E | 9.8–10.0 |

| Forward P/E | 8.0–8.2 |

| P/S | 0.84–0.88 |

| P/B | 1.50–1.57 |

| P/FCF | 11.7–14.4 |

| EV/FCF | 14.3–18.1 |

| Current Ratio | 1.72–1.79 |

| Quick Ratio | 0.66–0.82 |

| Debt/Equity | 0.45–0.48 |

| EV/EBITDA | 5.7–6.1 |

Performance

| Metric | Value (NOK) |

|---|---|

| Revenue | $15.62 billion |

| Net Income | $1.37 billion |

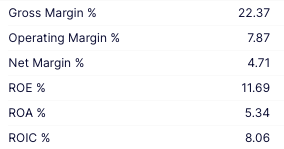

| Net Profit Margin | 8.76% |

| Operating Cash Flow | $2.48 billion |

| Free Cash Flow | $956 million |

| EBITDA | $2.46 billion |

| EBIT | $1.57 billion |

Subject to Urea Prices

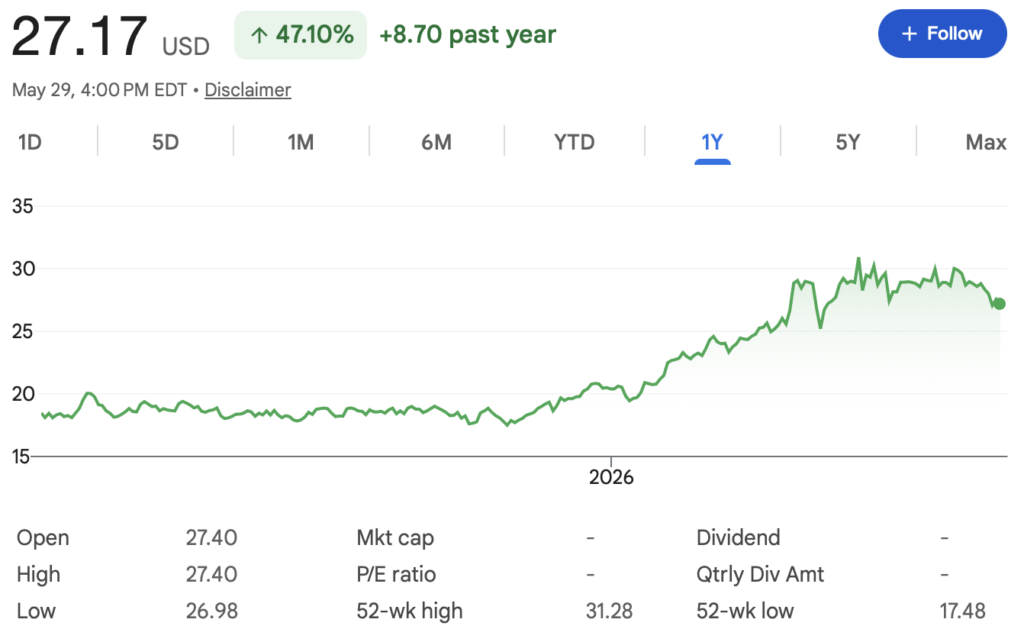

This is what first caught my eye. Below is likely due to the expectation of higher and higher performance amid higher urea prices. While it has pulled back, it has set a new, higher floor.

Uniqueness

Yara already has one of the world’s largest ammonia trading and distribution networks, including shipping vessels and import terminals. The company is attempting to plug that network into large-scale low-carbon ammonia projects, globally.

No Fertilizer, No Food

Price Range (52 weeks; NOK)= 365-497 (33-45 USD)

Shares outstanding (Million)= 254.73

I think its important to show the following, I’ve taken this screenshot years ago about the share price when the market was rather unexciting. Yet it still shows that its pricing is quite stable (more stable than bond prices as of late!).

Are you a writer who wants to earn from your ideas?

Balance Sheet

As of 2022, they had nearly 10B NOK in cash. Interestingly, for year end of FY2025, they also have around 10B NOK in cash.

| Metric | USD (bn) | NOK (bn) |

|---|---|---|

| Total Assets | $17.14B | ~NOK 181–183B |

| Total Liabilities | $8.39B | ~NOK 89–90B |

| Shareholders’ Equity | $8.74B | ~NOK 92–93B |

| Current Assets | $7.00B | ~NOK 74–75B |

| Current Liabilities | ~$4.30B | ~NOK 45–46B |

| Cash & Equivalents | $0.913B | ~NOK 9.7–9.8B |

| Gross Interest-Bearing Debt | ~$3.58B | ~NOK 38–39B |

| Net Debt | ~$2.67B | ~NOK 28–29B |

Trend

Recent disruptions in the Middle East have had an outsized impact on global urea and ammonia supply chains. Yara noted that roughly one-third of global traded urea flows are affected by the region, while Russian production has also faced disruptions. This is not all,

- Chinese export restrictions reduced global urea availability through much of 2025 and early 2026.

- Natural gas shortages continue to threaten production in regions like Egypt and Europe.

- India remains a huge importer and has been purchasing aggressively to secure supply.

The result has been:

- Higher nitrogen fertilizer prices

- Stronger ammonia margins

- Improved earnings for major producers

I’m not clear if this is assuming continued tightness in supplies or if it’s expressive of demand–however global fertilizer use is forecasted to reach record levels recently according to industry research.

Margins

And for Yara, as demonstrated in their Q1 2026 EBITDA jumped well above analyst expectations, helped by stronger nitrogen margins and operational improvements

| (USD) | Mar 2026 | Y/Y |

|---|---|---|

| Revenue | 4.22B | +16.55% |

| Net income | 326M | +10.88% |

| Net profit margin | 7.72% | −4.81% |

Yara has been a profitable company for the last 10 years.

The Divi

The current dividend is set at 15.86% and was forecasted to remain steady as such. It’s payout ratio is 128% TTM. Since, their share price has caught up a little, where it’s now at 4.38%

It’s 3-year dividend growth rate is 67.6%

5-year Yield-on-cost % is 66.25%

The Payout Ratio sits at 40.73%

Crucially for me however, is the incentive. Yara’s Annual General Meeting approved a NOK 22 dividend per share and renewed its share buy-back mandate, signaling that the board retains confidence in the company’s cash generation ability and commitment to rewarding shareholders over the coming year.

Debt Scare

Yara International had US$3.63b in debt in December 2025; about the same as the year before. However, because it has a cash reserve of US$913.0m, its net debt is less, at about US$2.71b.

While this looks awful, it’s less damaging since Yara International has a huge market capitalization of US$12.2b, and so it could probably strengthen its balance sheet by raising capital or line of credits, if necessary.

With net debt sitting at just 1.1 times EBITDA, Yara International is arguably pretty conservatively geared, especially for a commodity producer. And this view is supported by the solid interest coverage, with EBIT coming in at 8.9 times the interest expense over the last year. Even more impressive was the fact that Yara International grew its EBIT by 124% over twelve months. If maintained, that growth will make the debt even more manageable in the years ahead.

So far, management’s goals have been to focus on shareholder value creation, capital allocation, operational efficiency rather than deleverage any further.

To Conclude

Yara is a company with lots of debt on their balance sheet has previously made investors reluctant to jump for their shares, but now that is slightly turning around. Why? I believe it’s their unique exposure to urea & ammonia markets, both of which will continue to see price rises as a result of supply chain chokepoints and record consumption. They also continually produce ample amounts of net income and retain a steady high market cap–explaining their steady share price and consistent profitability.

Current investors are holding with the understanding that a stable payout ratio is in company strategy and returns on capital are the focus.

I believe this company has three appeals to it.

- It has been remarkably stable and uncorrelated to US or global equities which is quite hard to find. It serves as a great de-risk’er in ones portfolio in times of stress.

- Second, it has an ample source of assets and [in my opinion] will continue to see great profits as a fertilizer crunch occurs again and natural gas prices begin to rise off of their lows (despite it’s rise its still 72% below Aug 22 peak). Greater margins leads me to my last point–the dividend. Yara has paid a dividend every year since at least 2005, and I am not aware of any year since then in which the company completely suspended its dividend.

If you are adverse to “steady” bonds due to political, default, inflationary and/or interest rate risks, than if this stock can continue to hold steady and continue to pay (let’s say) a 6-12% dividend yield (far higher than bonds are paying in any Western/developed country) than this could be a great alternative.

Thank you for reading, be sure to sign up to the newsletter and consider subscribing for more stock reports

Email me with questions or if you’re interested in managed accounts services! Sea Lion Investment Office is ready for you