A Healthcare & Tech Trend

I first started thinking about this company after one of my times wasting time on the computer. I follow some accounts on Twitter (X) that periodically will list a number of sectors and some stock tickers–admittedly, there is nothing behind this other than the ticker and some empty promise that I’ll make millions. But–I often check out these companies just to see if there’s anything interesting that I feel like the masses are missing.

I believe the company below is one of those interesting companies. It is positioned to take advantage of a number of trends, which may be positive or negative, and supports this with a healthy balance sheet/signs of growth

Alast–my psychology degree was worth it!!

Company

Talkspace, Inc. is a behavioral healthcare company, which offers access to a fully credentialed network of licensed therapists, psychologists and psychiatrists. Through its platform, the company provides psychotherapy and psychiatry services to individuals, enterprises and health plans through both business-to-business (B2B) and business-to-customer (B2C) channels.

In talk therapy, members work with a licensed therapist or counsellor to treat specific mental health conditions, such as depression or anxiety, trauma and other human challenges, including by developing positive thinking and coping skills. In psychotherapy, the company offers text, audio and video-based psychotherapy from licensed therapists. In psychiatry, members receive personalized, care from a prescriber who specializes in mental healthcare and prescription management. The company offers its members a robust ecosystem for end-to-end behavioral healthcare.

Founded in 2012 by Oren and Roni Frank, Talkspace connects users with licensed therapists and psychiatrists through web and mobile platforms.

How it Profits

- B2B (Enterprise and Insurance): This is the company’s primary growth engine. Talkspace partners with Employee Assistance Programs (EAPs) and major health insurance plans to provide covered services to millions of members.

- B2C (Direct-to-Consumer): Individual subscribers pay out-of-pocket for various therapy tiers, offering high-margin recurring revenue.

- Strategic Partnerships: Collaborations with insurance payors have significantly increased the stock’s valuation floor by ensuring a steady stream of referred patients.

Financial

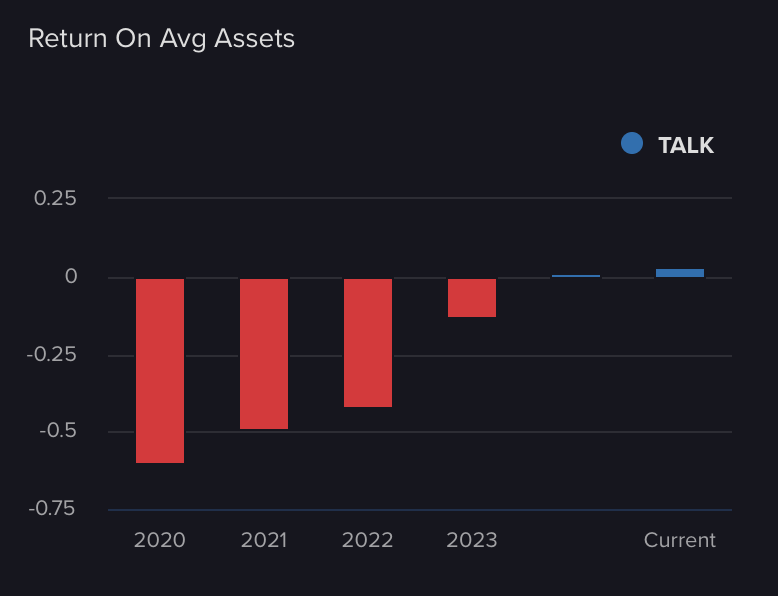

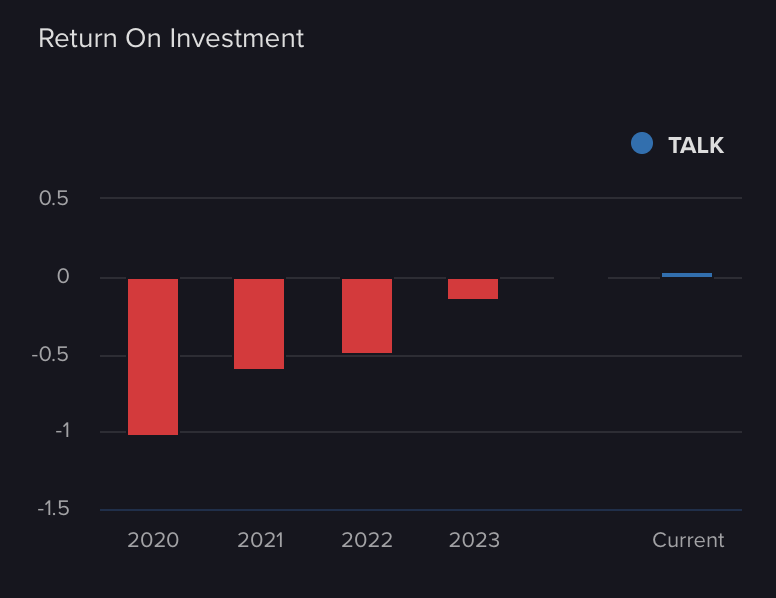

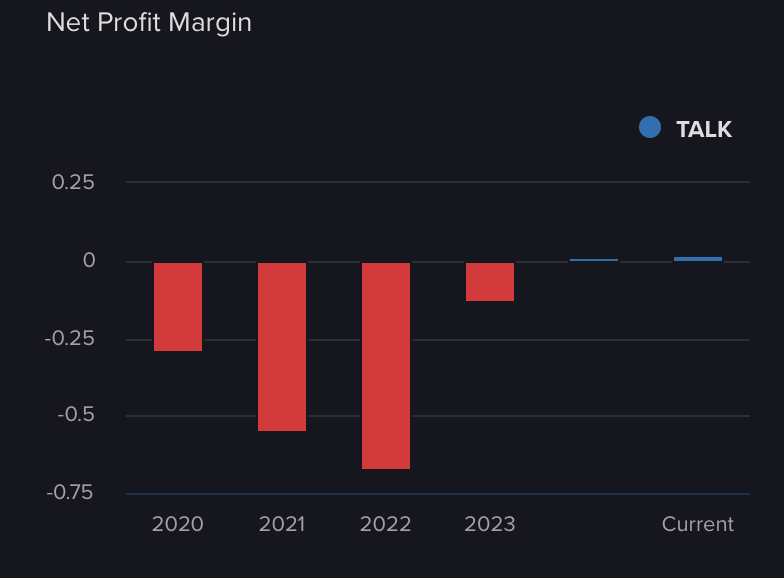

They are Rounding a corner... showing their return on avg assets, investment and their net margin, respectively (between 2-3%--small no doubt but compared to the last 5 years, they've made tremendous growth).

Their gross margin reliably operates at 42% year over year. This has allowed them to grow their EPS by 378.21% in their latest numbers while the industry average sits at 4.7%

What caught my eye was if we go back to 31 March 2024, Talkspace Inc revenues increased 36% to $45.4M meanwhile their net loss was decreasing 83% to $1.5M. Revenues reflect an increase in demand for the company’s products and services due to favorable market conditions as opposed to one-off conditions. Lower net loss reflected research & development decrease of 34% to $3.1M (expense), interest Income increases from $600K to $1.6M (income) and a sales & marketing decrease of 4% to $12.6M (expense).

Talkspace presents a compelling growth story with earnings forecast to grow 46.9% annually and revenue expanding 17.1% per year, significantly outpacing market averages

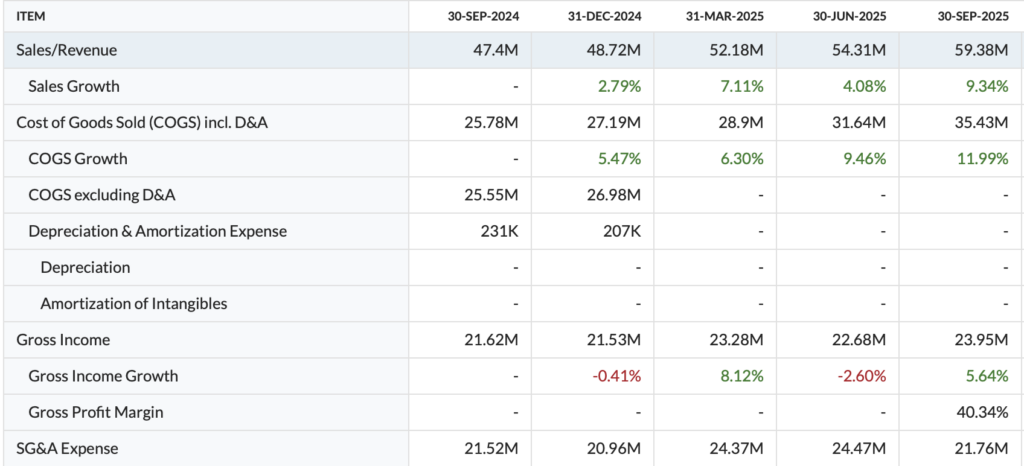

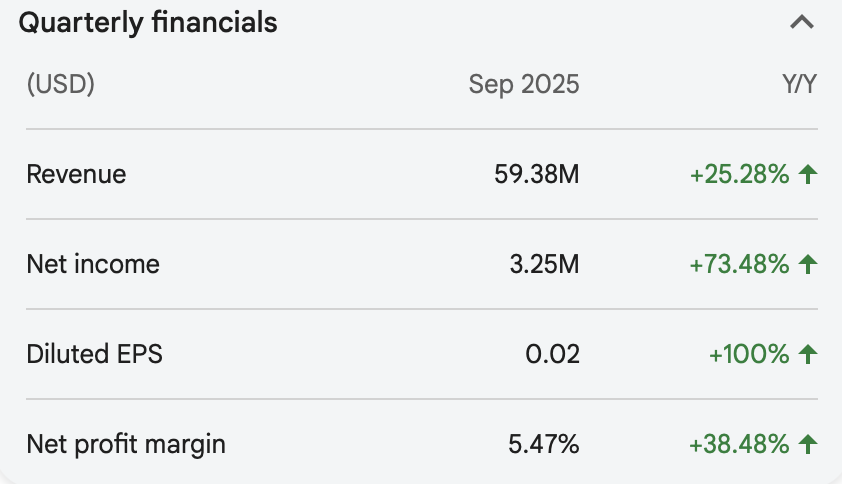

This trend has continued if we fast forward to present:

Note that the SG&A is steady, with incremental increases to their sales. Their COGS also have been increasing, but I believe the important part is that they are demonstrating adoption onto their platform and once you see their balance sheet you’ll see that it’s nothing to be worried about.

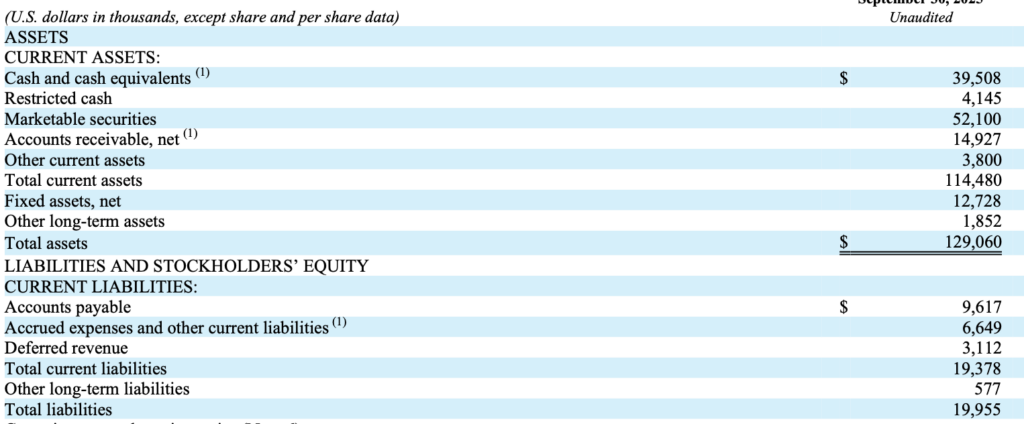

Balance Sheet

Strange for a tech-oriented start up type business but they have the opportunity to utilize their cash alone to cover all of their total liabilities including their accounts receivable.

Business Advantages

Talkspace operates a virtual mental health platform connecting patients with licensed providers via messaging, audio & video — a sector with strong secular demand thanks to rising awareness and need for accessible mental healthcare.

- Behavioral health services are no longer niche — this is a growth vertical within healthcare that many traditional providers are only beginning to embrace. It’s a relatively new field in the vast healthcare sector.

- The company has cleverly hooked itself to existing insurance providers to create an enormous scaling potential. Talkspace isn’t just selling therapy apps — it contracts with health insurance plans, Medicare Advantage networks, and enterprise clients such as with Amazon Health Services

- This means covered lives — people whose insurance could pay for Talkspace services — has grown into the hundreds of millions of Americans. This has created a massive upside potential.

- This provides a scalable distribution engine. The more insurance coverage it is able to acquire, the bigger its potential customer base.

- Their business is inherently far less capital intensive than a pharmaceutical company. In the business itself, we have far more potential for revenues than we do added capital costs.

Interestingly, they’re also utilizing the rise of machine learning and integrating AI tools to improve provider workflows and user matching with appropriate specialists as per their most recent filing.

Points to Consider/Macro Market

- There is absolutely no sign that United States citizens’ mental health is improving (On The Ball believes that the United States has far exceeded the stages of demoralization, destabilization and is in a perpetual state of chaos; leaving citizens to manifest chaos, abnormal thought and psychoses in their day to day lives.

In other words, it can be said that a majority of the country are victims of psychological warfare and are abnormally, abnormal (if this makes sense) which creates a larger than expected pool of clientele. TALK are looking to exploit the growth potential in a large, under-penetrated healthcare segment. - Digital…is the future. Just because we may be terrible at operating software code or figure out how to turn the brightness down on a tablet… doesn’t mean otherwise. The younger generation, identifies with technology more than any other before it. In fairness to them, it’s nearly impossible to operate/keep up without having some sort of technological identity/device stamped to you. But, again, from a longer-term perspective it’s that younger generation who will be more likely to adopt a digital interface for mental health service than the baby boomers. The Zoom culture has probably annoyed the hell out of millions…but it’s now established itself as normal.

On The Ball writes macroeconomic, contrarian, global trend and travel posts…but also has nearly 100 stock pick recommendations

A Closer Look for Potential Problems

- Total Debt/Total Equity 0%—- 5Y Avg: 0% Industry Avg: 50.8%

Total Debt/Total Assets 0%——- 5Y Avg: 0% Industry Avg: 25.09%

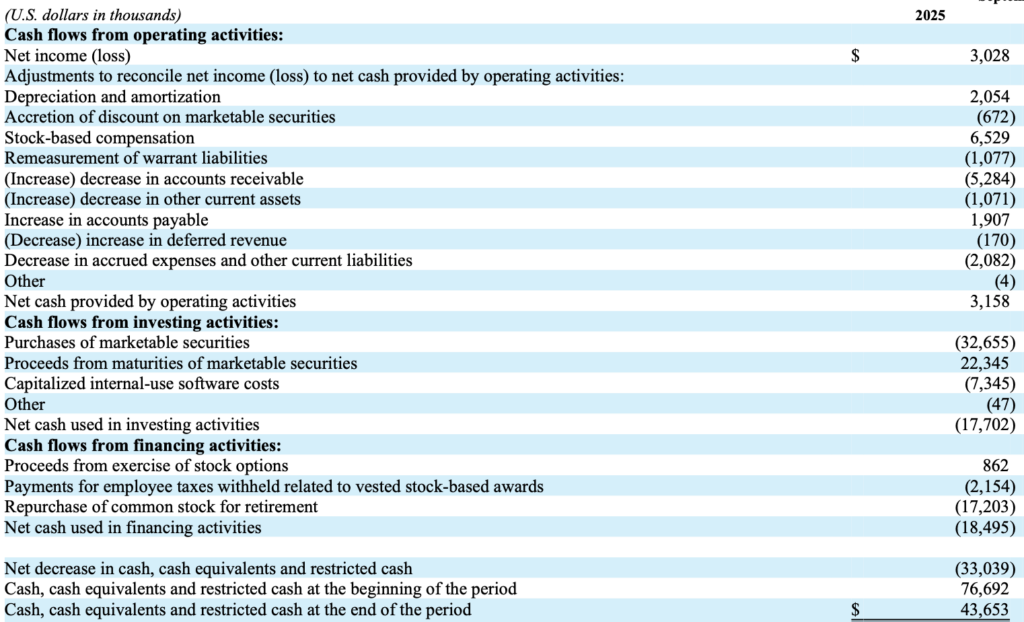

Nothing interesting on cash flow (anything you should be worried about)

The takeaways here are that a significant amount of their cash flow is dedicated towards investing activities, of which, pays a significant return for the quarter. Other than that, they’re able to generate a quiet net income and keep operating activities very modest. It’d difficult to go through these reports and get the sense that management are looking to squeeze equity out of investors.

It’s worth mentioning the high valuation metric since the stock trades at an expensive P/E ratio of 138-147.6x, more than 3.5 times the market average of 39.83x. This premium valuation makes the stock vulnerable to any earnings misses or growth disappointments (but growth is higher than the market average too)

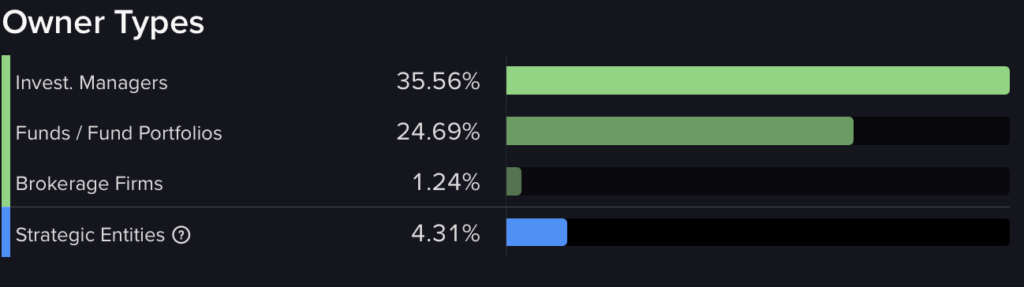

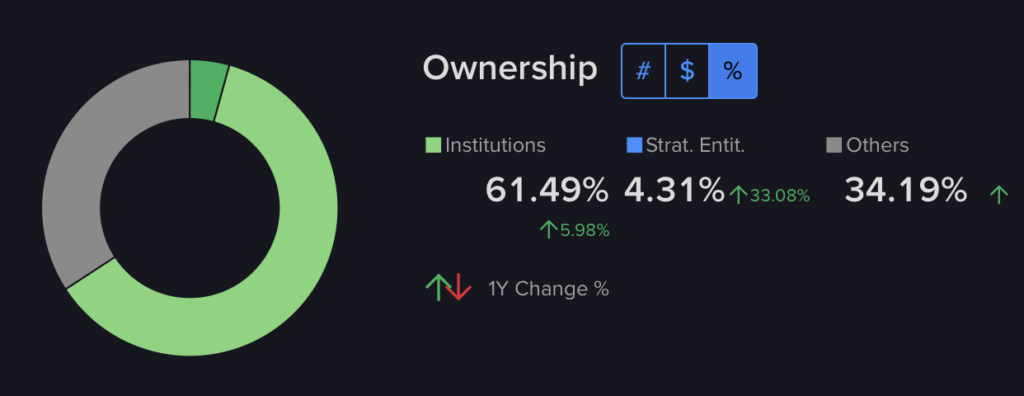

Ownership

This company is majority owned by institutional fund managers…which I believe, if we’re looking at this from a longer term perspective is interesting for two reasons:

1. The company received the “big money” blessing already as having sound investment prospects and growth potential and yet;

2. So, so many of these institutions are over leveraged and holding onto bad assets that they’ll be forced to exit lots of their book to free up capital… creating a buy opportunity for you and I.

Interestingly, they have launched their own share repurchase program, too.

The Company announced that its Board of Directors approved a share repurchase program to authorize the repurchase of up to $15.0 million of the currently outstanding shares of the Company’s common stock over a period of twenty-four months beginning on March 1, 2024.

On August 1, 2024, the Company’s Board of Directors amended the Share Repurchase Program to authorize the Company to repurchase up to an additional $25 million of its common stock for a total of $40.0 million. The Share Repurchase Program will remain in effect until the earliest: 1) the total authorized dollar amount of shares is repurchased or 2) August 1, 2026.

During the three and nine months ended September 30, 2025, the Company repurchased and retired an aggregate of 3,516,677 and 6,577,115 shares, respectively. As of September 30, 2025, $11.8 million remained available under the Share Repurchase Program.

To me this is very interesting given how they are only recently and modestly profitable.

Risks

Right now, many niche healthcare stocks are on the way down despite having fantastic market potential and/or flawless balance sheets providing them a runway for takeoff. There’s a chance that TALK falls with the entire sector–especially as the bubble continues to burst in broader, “mainstream” equities. I personally view this as a great thing as it creates a bargain.

Another obvious risk is the regulatory environment: Compliance with HIPAA and varying state-specific mental health regulations can impact operational costs and delay specific guidance expectations.

Losing various insurance agreements could also be a major hit to their potential upside as well, though I can’t find any risk of this reported.

The business model still faces questions about scalability and sustainability, with ‘ifs, buts, and maybes’ surrounding its ultimate success–but this is where the risk:reward ratio pays for us.

Closing

Talkspace, inc. is a relatively unknown company supporting a market cap of 664M USD that is positioned to take advantage of the technological world, a healthcare crisis and current institutional support.

The transition to a payor-focused model with Medicare and TRICARE expansions has driven remarkable growth, with payor revenue surging 42% year-over-year in Q3 2025. Completed payor sessions increased 37% and active payor members grew 29%, demonstrating strong customer adoption and establishing a stable growth trajectory.

On the downside however, we can’t ignore the fact that there is an immensity of regulation, it’s high valuation numbers at the moment (though as I said I believe these will improve in the future) and the uncertainty of receiving further users/insurance contracts.

This company is truly a growth play rather than a value play given that its net income margins are only thin and its valuations are not a bargain. Still, I very much like this company

- They’ve reached profitability and have dozens of quarters of increased growth with further growth forecasted; not only this– but they’ve extended their share buyback program

- They have a cash position that nearly doubles their total liabilities providing a major runway for revenues to continue to grow

- They’re in a low cost field, with established insurance relationships + Medicare and TRICARE expansions

- Crucially, I believe the macro trends of poor mental health outcomes coupled with the normalization of online business interactions is a generational advantage this company has moving forward

We’re looking at a company that may fit a major piece of the puzzle for your portfolio given the following. It may be prudent to wait until the share price can be picked up around $2.50-$3.00 for a cheaper entry point–but I’m of the opinion that this company is going a lot higher as the revenue pours in and their balance sheet is further strengthened while competitors are struggling to refinance their bloated balance sheets amidst market turmoil.

What do you think?