Company

The Western Union Company is an American multinational financial services corporation headquartered in Denver, Colorado. I was surprised to see that it is a rather old company having been founded in 1851.

Investment Themes

Financial Services

Core operations are centered on financial services, with a focus on accessible financial solutions and cross-border, cross-currency money movement, including bill payments, money orders, foreign exchange, prepaid cards, lending partnerships, and digital wallets.

Payment Solutions

Core business operations heavily rely on payment solutions, focusing on cross-border, cross-currency money movement, bill payment services, and user experience enhancements through digital platforms and account payout networks.

Digital Wallets

Involvement with digital wallets is demonstrated through the Consumer Services segment, strategic partnerships like those with urpay and du Pay, and the launch of a new digital wallet offering in Australia.

Consumer Finance

Core business activities demonstrate a focus on consumer finance through accessible financial services such as bill payment, money orders, foreign exchange, prepaid cards, digital wallets, and lending partnerships, aiming to lead in cross-border, cross-currency money movement and payments.

Mobile Payments

Facilitation of money transfers through websites and mobile devices, including partnerships with digital wallets like urpay and du Pay, indicates involvement in mobile payments.

Retail Segment

Involvement with the retail segment is evident through consumer money transfer services via retail agent locations, with strategies to rationalize the retail footprint, enhance value, and improve customer experience, while also offering retail foreign exchange services and aiming to grow market share.

Credit & Lending

Engagement in credit and lending is evident through the Consumer Services segment’s lending partnerships, management of credit and fraud risks, and the impact of credit losses on service costs.

Ratios

| PE Ratio | 2.83 |

| Forward PE Ratio | 4.97 |

| PE Ratio without NRI | 5.16 |

| Shiller PE Ratio | 4.87 |

| Price-to-Owner-Earnings | 7.35 |

| PS Ratio | 0.64 |

| PB Ratio | 2.97 |

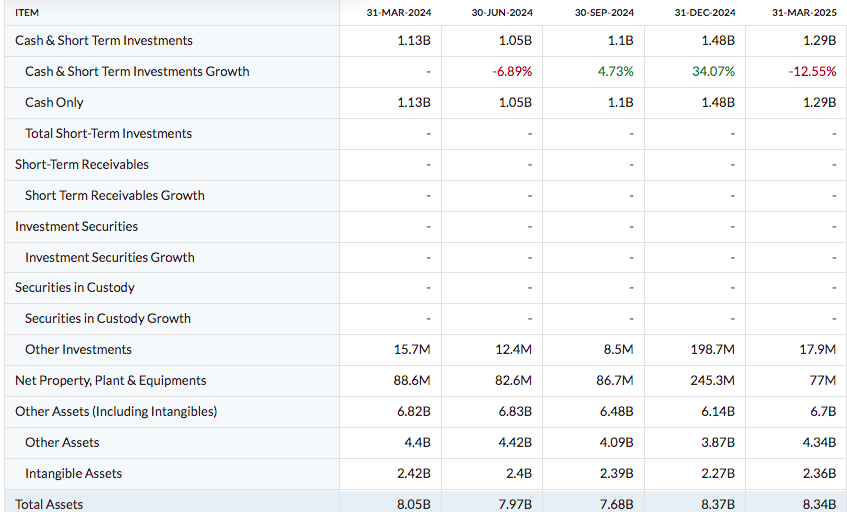

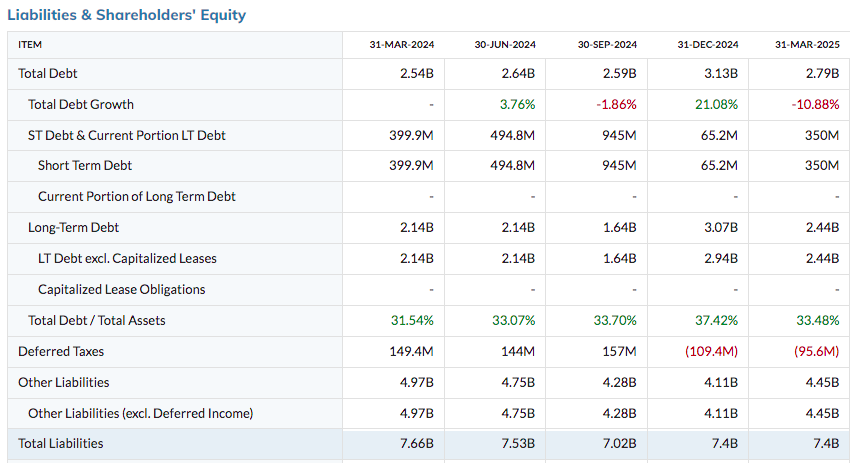

Balance Sheet

Looking at this, you can see while they have a significant amount of debt though it is long-term, the short term debt is more than handled by total cash reserves; it is also handled well against total assets. Their other assets nearly cancels out their other liabilities as well.

Dividends

Performance (Q2 2025 unless stated)

GAAP revenue was $1.03 billion; down 4% on a reported basis; adjusted revenue,

excluding Iraq, was down 1% (slowdown from weakened US profits, explaining their acquisition below)

Branded Digital revenue grew 6% on both a reported and adjusted basis, with

transactions up 9%

Consumer Services reported revenue grew 39%; adjusted revenue was up 41%

GAAP EPS of $0.37, or adjusted EPS of $0.42

Segments and increase/decrease

Consumer Services segment revenue grew 39%

Branded Digital revenue increased 6%

Consumer Money Transfer segment revenue decreased 8%

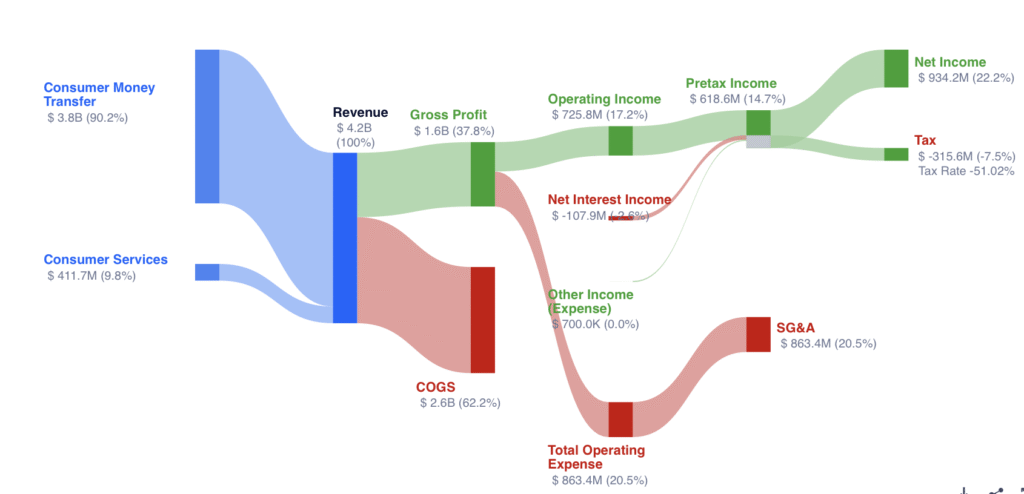

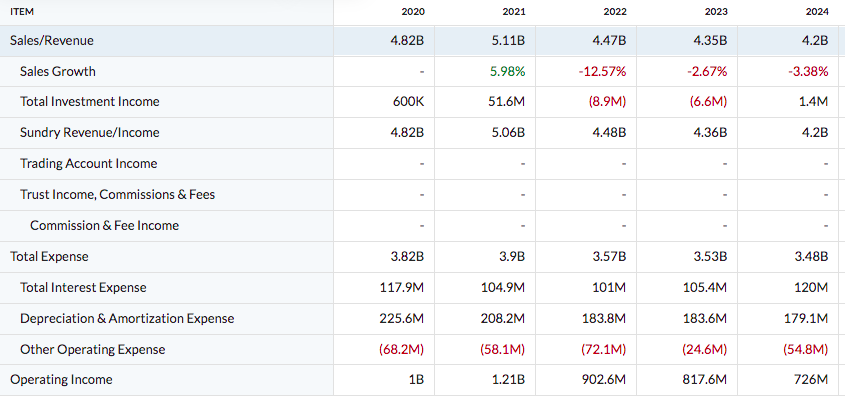

Interestingly, quarterly their operating expenses has fallen by 4%, SG&A fell by 8%, and their provision for income taxes for this quarter (year too) has been much higher, explaining a chunk of reduced net income.

Very Interesting

- Western Union has made a management decision to buy back stock aggressively at these low prices, with a $1B buyback reducing share count by 15%

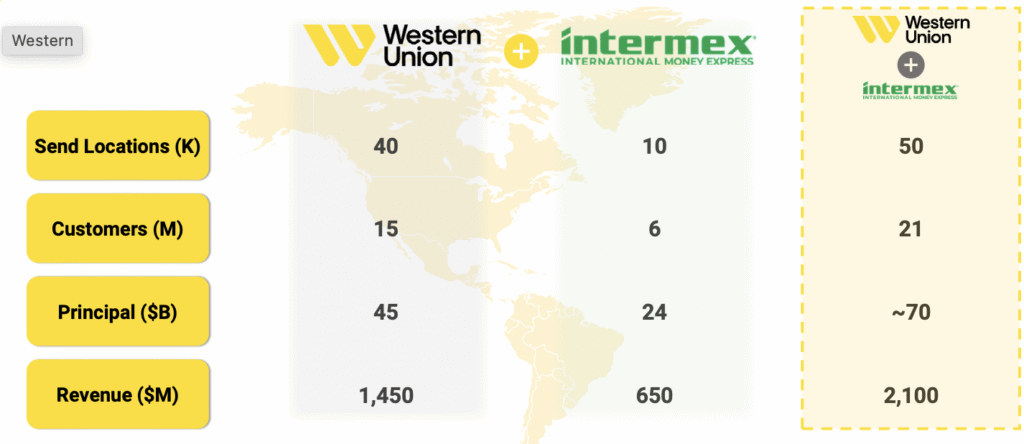

- They have acquired Intermex Money Express a few months ago in a definitive agreement under which Western Union will acquire an all-cash transaction at $16.00 per IMXI share, representing a total equity and enterprise value of approximately $500 million. The move was to expand Western Union’s retail offering in the U.S. market coverage. The reasoning was to acquire: “a well-positioned remittance business, adding scale in historically high-growth Latin America geographies. It is an opportunity to serve Intermex’s 6 million customers, giving them access to Western Union’s robust digital platforms and capabilities” Intermex revenues for 2024 were $658.6 million across more than 10,000 locations in the USA.

- Western Union operates in over 200 countries and territories, with more than 130 currencies supported. That is an immense amount of scale.

- Not falling behind on the digital transformation front. They’re trying to target the digital methods in emerging markets as part of a strategy, with lots of room to grow yet.

Further Look

Their other assets (which essentially cancels out other liabilities) entails:

1. Derivatives (financial instruments): e.g., foreign-currency hedges recognized under “other assets”.

2. Non-settlement long-term assets: such as long-term unbilled receivables and deferred charges.

The intangible assets is mostly in the form of goodwill (Goodwill: $2,059.6 million — the excess paid over underlying fair value in acquisitions). Their deferred taxes is a nice benefit.

Business

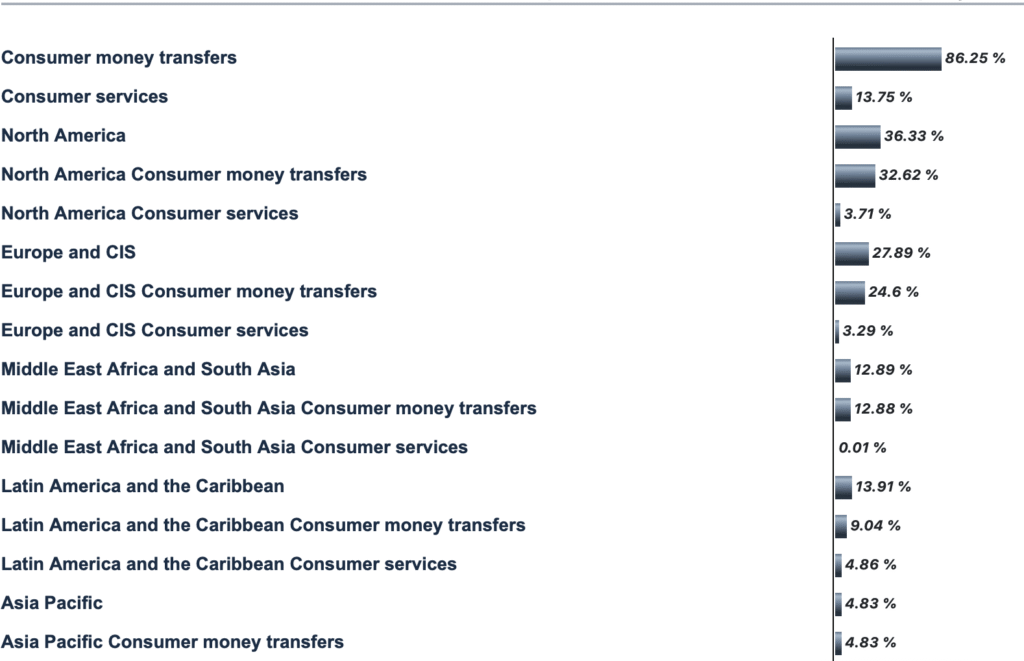

85% of their businesses are customer-to-customer services split between 6 different methods; only around 15% of their business is customer-to-business.

Side Note

Western Union stands to benefit from the continued exodus of people and their capital to foreign countries around the world–I can only speak to Paraguay & Mexico but they are the most cost efficient method of moving money from Mexico, Canada and England to Paraguay and the United States, aside from cryptocurrency of course.

You can bet that they will be subject to some sort of capital control which may hurt future growth potential, but this may be offset by the “unexpected” amount of new users in the relatively near future that markets will overlook.

Chris MacIntosh, hedge fund manager and newsletter writer always says “Find the narrative that is incorrect and bet against it”. I believe that the narrative that capital and people won’t be on the move within the next 10 years is fundamentally an incorrect narrative that will fall flat once all of these major events (sovereign debt crisis, wars, civil unrest, complete tyranny, digital currencies and so on) take shape. In fact, here’s two instances of me covering this already.

Trend is Lower

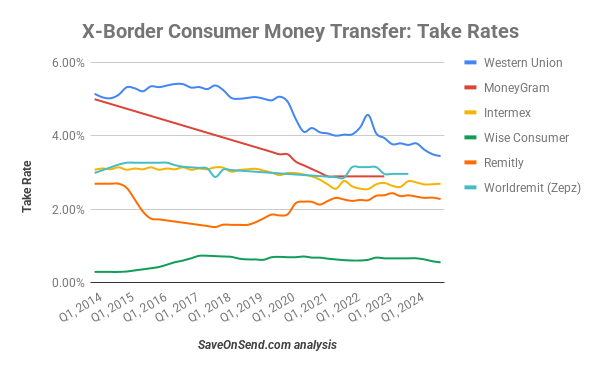

You can see that while expenses are falling, too there is a negative trend in overall growth and operating income from years prior. I believe that this is related to the recession that has occurred in the real-economy but not hit the S&P 7 which means general equity markets.

Perhaps in the case of Western Union however, its continual downfall lower than the 2008 lows are more related to policy making uncertainties rather than a downfall in absolute demand.

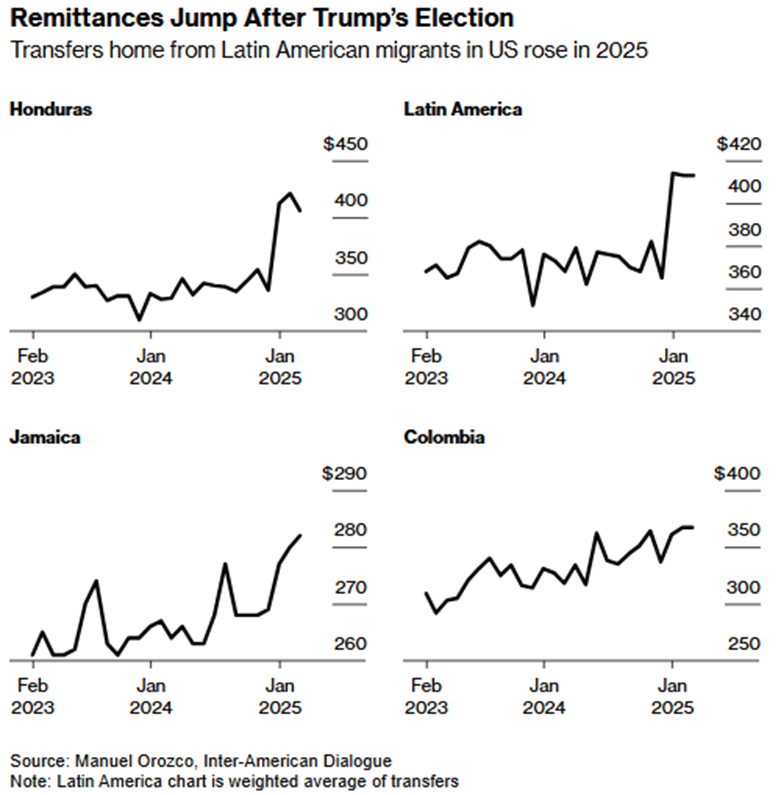

“Immigration Policies” through Trump’s insistence to weaponize ICE against everybody can be seen as a threat since a lot of the money leaves U.S. to head to ➔ Mexico, Guatemala, Honduras, Colombia, etc. Anecdotally, from a Mexico perspective, I can only say that immigration procedures are more expensive but that most already in the United States are continually to send money home. I think this will pass, and most is political posturing related to larger matters at play.

Western Union expects a $30 million in cost savings within 24 months after the Intermex purchase

Stablecoin Craze

Some have said that Western Union is going bankrupt, why? Due to cryptocurrency.

The fact of the matter is that very few, today use cryptocurrency as a means of purely transactions for purchase; rather it remains a tool for speculation/trading and HODL’ing. I don’t doubt the rise of Stablecoins will take away some profits from Western Union, but they are greatly hedging this risk themselves by…creating their own!

Western Union joins stablecoin race, eyes crypto partnerships: CEO

Western Union is exploring stablecoin integration for cross-border transfers, conversions and digital wallets, positioning it as an innovation opportunity.

They are trying to act as the bridge between traditional finance and crypto that is allegedly occurring (I have my thoughts). Pilot programs begin in Latin America in Q4 2025, with global rollout planned for 2026.

Big Buy

Advantage

The primary user base of MTOs consists of migrant workers and blue-collar customers, with very low value-per-customer — less than $500 at Western Union. These small-ticket transactions often fall under simplified due diligence thresholds, allowing companies like WU to operate without building full KYC/AML systems. It may be worth noting too that an amount this low may be under thresholds made on future capital controls (remains to be seen). By contrast, direct integration with national payment systems requires comprehensive audits of all KYC/AML processes before licensing is granted. In other words, this means more and more expenses that greatly tap into net margins.

It’s worth noting that Western Union won’t face new competitors anytime soon as the legal rats nest of this industry simply isn’t worth it if one were to start out today.

Closing

We’re looking at a stock that uses its FCF to support high dividends and trades for less than 5x earnings. The business has been a lot more steady than you might think, having been around for more than 170 years in the big picture and a short-term picture of recent consecutive revenue growth records by quarter. Western Union is a global business in nearly every country on the planet; owning it, is largely a diversified financial play.

While I don’t think stable coins are going to be a threat for Western Union, if anything, they’ll enable them further growth, I think there is still the threat of capital controls which can hurt revenue expectations (despite a huge amount of immigration continuing despite what headlines read). The fact of the matter is that immigration is continuing, albeit at a slower pace and we’ve just had the transfer of 10s of millions of people around the world in recent years.

In the meantime, we’re left with a company trading at sub 3X earnings, proven resilience for over 150 years, paying a dividend between 7-11%, with added new exposure to US markets and a manageable balance sheet. It would seem that fears floating about suppressed this stock a little further than what it otherwise deserves to trade. This stock looks to be an opportunity to me; with the caveat that certain news events could send the share price falling sharply. In the event of capital controls, the dividend is a nice little hedge from a potential continued weakened revenue figures, which provides investors an opportunity to sell if they desire (RELY another company I like, doesn't pay a dividend). Otherwise, it’s a predictable business with free cash flow.

Please do your own due diligence before taking actions–you know the drill!

For more stock picks, macro topics and geopolitics (+ new companies we're launching) consider subscribing!

#StayOnTheBall