Company

Here’s a company I accidentally came across after writing in a ticker wrong (yes, really). I immediately was perked up by some of their numbers bit by bit like that Vince McMahon meme.

Then I noticed the following…

% OF FLOAT SHORTED is 23.86%... what on the earth is going on?

However I finally found why everyone wasn’t jumping for it

The ~23–26% short float on CorMedix is unusually high, but it actually makes sense once you look at the situation around the company. It’s not just random — there are a few specific reasons shorts are targeting it.

But Hang On…what’s exactly going on here? Are the Hedge Funds wrong? What are they betting on exactly?

First, please subscribe to On The Ball by leaving your email or if you want strategic capital advisory OR investment management, get in touch privately via the Contact Page. Thank You

Lets Go Over The Good Things

Fundamentals are strong

It is a company that is:

- profitable

- has multiple drug products

- great valuations

- great balance sheet

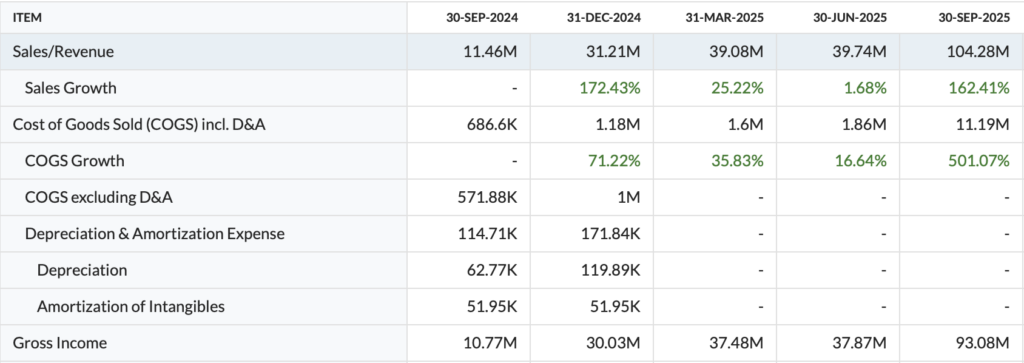

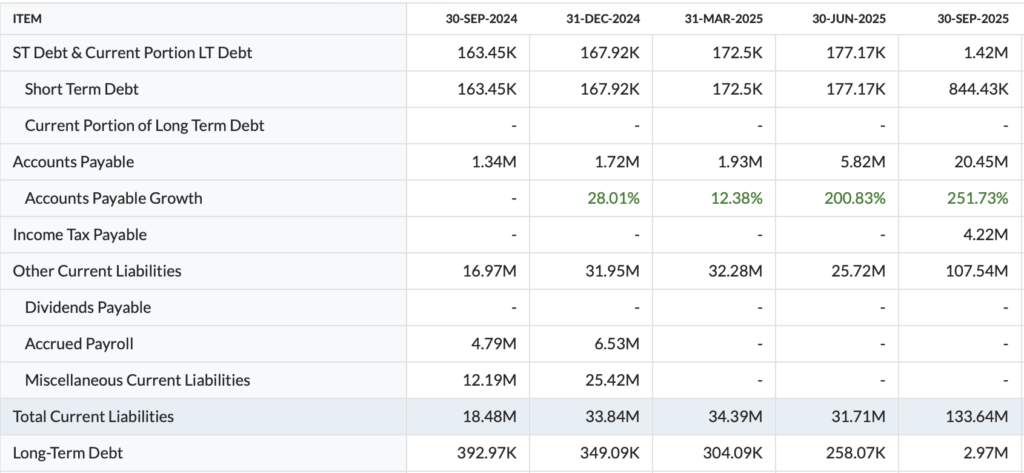

Balance Sheet

The other current liabilities are simply accrued expenses from their most recent acquisitions

1️⃣ Milestone / acquisition-related payments

2️⃣ Sales-based royalties and distribution fees

3️⃣ Sales rebates / chargebacks

4️⃣ Compensation and bonuses

Total Liabilities/Total Assets: 50%

Again, on the surface it looks like a stock thats beaten up–been there done that, and totally out of favor as being left for dead.

Products

Full CRMD product list (current)

1️⃣ Core CorMedix drug

- DefenCath – dialysis catheter infection prevention

- flagship product

- main revenue driver

2️⃣ Drugs added from the Melinta acquisition

These are mostly hospital anti-infectives.

Antifungal

- Rezzayo (rezafungin)

- treats invasive Candida infections

- possible expansion for transplant infection prevention

- Phase III data expected 2026

Antibiotics

- Minocin IV – IV minocycline antibiotic

- Baxdela – antibiotic for skin and bacterial infections

- Vabomere – resistant gram-negative infection antibiotic

- Orbactiv – long-acting antibiotic

- Kimyrsa – improved version of Orbactiv

These are sold mostly to hospitals and infusion centers.

Cardiovascular drug

- Toprol‑XL

- extended-release metoprolol

- used for high blood pressure and heart failure

This one is actually an older blockbuster drug originally developed by AstraZeneca decades ago, but Melinta owns the U.S. rights now.

CorMedix revenue by product (2025)

Total revenue 2025:

$311.7 million

DefenCath

Main product for dialysis catheter infection prevention.

- Revenue: $258.8M

- Share of total revenue: ~83%

This drug is used after dialysis to prevent bloodstream infections from catheters.

Melinta antibiotic portfolio

(Acquired in 2025 when CorMedix bought Melinta Therapeutics.)

Revenue: $52.9M

Share of total revenue: ~17%

These are multiple hospital antibiotics sold together as a portfolio.

Main drugs in that group include:

- Vabomere – antibiotic for resistant infections

- Orbactiv – skin infection antibiotic

- Minocin IV – IV minocycline antibiotic

- Kimyrsa – newer long-acting antibiotic

CorMedix does not report revenue separately for each one, only the combined “Melinta portfolio.”

Revenue Upside Important pipeline (not revenue yet)

These are not generating revenue yet, but they are potential catalysts:

- DefenCath expansion

- Rezzayo antifungal prophylaxis: It’s currently approved for fungal infections but is being tested for prophylaxis in bone marrow transplant patients. If the Phase III trial succeeds: potential >$200M peak annual sales. That would make it the second major product after DefenCath.

- pediatric dialysis indication

If any of these hit, revenue diversification increases…But the data isn’t out until late 2026.

The Melinta portfolio actually used to generate about $120M+ revenue before CorMedix bought it, which means CRMD suddenly became a profitable multi-drug company overnight after the acquisition

Bullish view

The transition year creates a temporary headwind, but the longer-term earnings potential of the combined platform remains undervalued. DefenCath continues as a core value driver with significant market opportunity estimated at $500-750 million in TPN indication alone, and the current low P/E around 3x doesn’t reflect consensus expectations of 52.8%

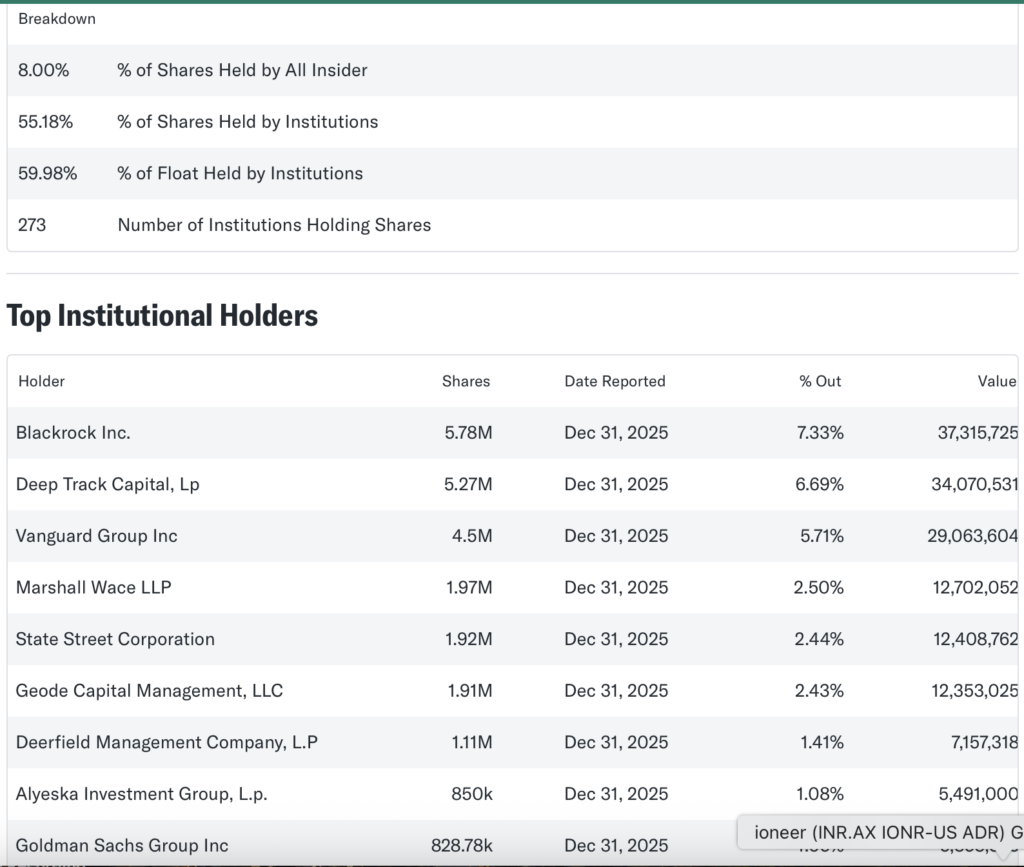

Ownership

Strong institutional ownership already

Other Side: The Hedge Funds Shorts

Some reasons:

1. Single-product biotech risk

CRMD can be argued to be basically a one-drug company.

Their revenue depends almost entirely on DefenCath, used to prevent infections in dialysis catheters.

Even though they technically sell 5+ drugs, the economics look like this:

DefenCath = the entire business.

Roughly:

- 83% of revenue

- nearly all growth

- main profit driver

Short sellers love single-product biotech companies because the downside scenario is easy to model.

2. Reimbursement uncertainty (biggest issue)

The real fight is reimbursement from Medicare dialysis systems. DefenCath currently benefits from a special payment program: TDAPA

This program temporarily pays dialysis centers extra for new drugs.

Under the Medicare dialysis payment system:

- TDAPA lasts about 2 years for new dialysis drugs. During this time Medicare pays ~100% of the drug’s average sales price.

For DefenCath:

- TDAPA started July 2024

- Expected to end mid-2026

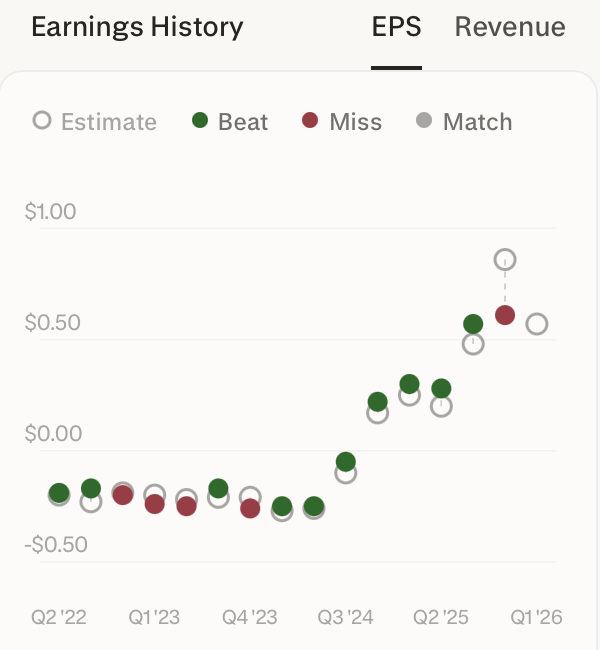

After that the drug transitions to a different reimbursement structure. FY26 revenue guidance sits roughly 40% below prior Street expectations, with 2027 DefenCath guidance at approximately half of some earlier estimates.

The problem:

If reimbursement drops, dialysis providers might stop using it or at least this uncertainty could crush quarterly revenues.

This uncertainty is one of the main reasons bears short the stock. Furthermore, a loss of these agreements would be impactful give that revenue is not only concentrated by product but also by customer.

One filing showed:

- Customer A → 33% of sales

- Customer B → 26%

- Customer C → 23%

That means three customers = ~80% of revenue.

3. Stock already ran hard

CRMD had a huge run after commercialization, if you look at their prior stock price above, you can see that it’s not shaping up as a company “ready to break out” anytime soon.

4. Volatility attracts blood

The largest short positions are reportedly from trading firms like:

- Citadel Advisors

- Susquehanna International Group

These firms often short biotech momentum runs or run market-neutral strategies (long biotech ETFs, short specific names).

There are three interesting things going on with CorMedix (CRMD) that explain both the Melinta portfolio strategy and why some hedge funds are skeptical.

Will the Melinta portfolio actually grow?

The drugs of Rezzayo, Minocin, Baxdela, Toprol-XL, etc. — came from the 2025 acquisition of Melinta Therapeutics.

Before the acquisition:

- Melinta generated about $120M revenue in 2024

- Expected $125–135M in 2025

So the expectation is low growth, not hypergrowth.

What management thinks

CorMedix expects:

- cost synergies: $35–45M annually

- EPS accretion in 2026

- a stable hospital drug platform (CorMedix)

Short sellers are betting on one of these things breaking:

1️⃣ dialysis reimbursement changes

2️⃣ adoption slows at dialysis chains

3️⃣ Melinta drugs stagnate

4️⃣ Rezzayo trial fails

Because if DefenCath demand slips, the company loses most of its revenue base.

But here’s the bullish counter-argument

If DefenCath adoption keeps expanding across dialysis centers and their loss of TDAPA is handled carefully.

Some analysts think DefenCath alone could reach:

$700M–$1B annual sales eventually.

If that happens:

- the current market cap would look extremely cheap.

Closing

To Summarize…

CRMD is a very unusual small biotech:

- profitable

- multiple drugs

- but one drug + a few customers drive everything

That combination explains the ~24% short interest.

This company may very well be one of the first HOLD recommendations from On The Ball. While I tend to favor their balance sheet, current share price and slow upside of their newly acquired portfolio will edge up the company in value–it’s hard to overlook the fact of how reliant they are on one product, amongst a few customers with lots of competition out there and weak immediate growth prospects.

I can understand one wanting to short this company on the trade that this is going to break whereas I can understand someone playing the long game that these shorts unwind and their product expansion pays off.

My advice? Really hold out on this one to see how it plays out.