Temporarily Available For Non-Subscribers

Company:

Performance Shipping Inc is a Greece-based global provider of shipping transportation services. It owns containerships and focuses on providing sourcing opportunities for vessel purchases and sales, new building acquisitions, chartering and financing arrangements. The Company’s vessels are employed primarily on charters with liner companies carrying containerized cargo along worldwide shipping routes. The Company owns and operates vessels such as Panamax container vessel and Aframax tanker vessel. The Company’s fleet is managed by Unitized Ocean Transport Limited, a wholly owned subsidiary. The Company’s customers include national, regional and international companies. Performance Shipping Inc. employs its fleet on spot voyages, through pool arrangements, and on time charters.

As of June, 2025 the Company owns and operates six Aframax tankers, as well as three newbuild LR2 and one newbuild LR1 tanker vessels, with scheduled deliveries ranging from 2025 and 2027. The company financialized the sale of “P. Yanbu” ship in March 2025. The total value of their ships is estimated to hold an asset value of $488.9M.

They hold a total deadweight of 630,519 and their trading ticker is $PSHG on the Nasdaq.

Share Price

The share price has become murdered in recent years.

-Performance Shipping has raised $37.7 million over the past 13 months from diluting common shareholders well below NAV. This had left a sour taste in the mouths of investors.

-The stock the last 5 years is down over 98%… it has absolutely bottomed out and you’re buying it extremely cheap (as I’ll show)

-The new shipbuilding contracts are great but they are relying on China for the next three years. This leads to geopolitical and economic concerns on China’s willingness or capability to fulfill these contracts in a timely manner (realistically, likely not worth the terrible share results…especially as you read on).

-Preferred stock pays out ~4.5% and accounts to around 9% of outstanding shares (some felt like that the deal was much greater than the publicly stocks, though I’m not sure how).

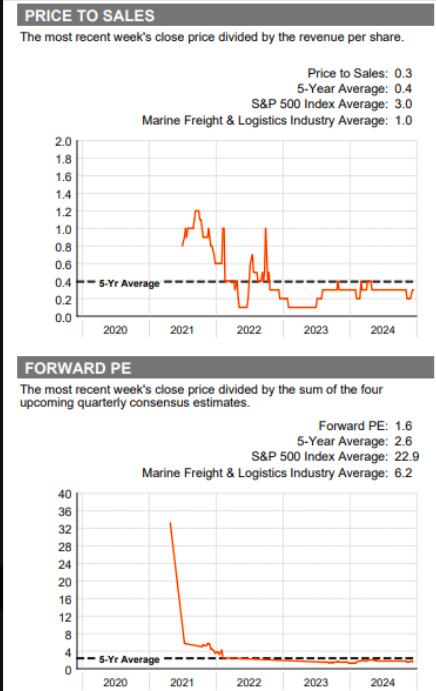

Ratios

P/E: 1.2

P/B: 0.10

P/EPS: 1.0

P/E/G: 1.79

Cash on hand: $68M (+ Performance Shipping (PSHG) reported a cash balance of approximately $192 million as of July 30, 2025, following a $100 million bond offering).

EPS: 4.83

Net Loan to Net Value Ratio: -26%

Market Cap: 22.25M (note this difference)

8% of the float is currently being shorted.

Please give a follow on LinkedIn and keep an eye out for new job postings: https://www.linkedin.com/in/matt-b-5928512b8

Numbers Don’t Add Up…

EV/EBITDA: 8x

EBITDA: $74M → Implied EV: $592M

Net Cash: $52M → Equity Value: $644M

Shares: 12.43M

→ Fair Value: $51.80/share

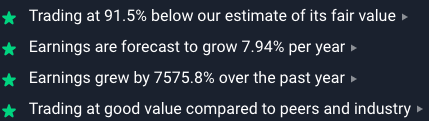

Just on NAV alone, we’re looking at a $25 share price.

but now… the Market Price is only $1.89

- If you look of their 4 newbuilds that are coming due in the next 2 years…they hold a total Construction Cost of $249.5 million while the Fleet-wide Revenue Backlog stands at $220 million representing 118% of all remaining newbuilding capital expenditures… In other words, they’re nearly getting 4 newbuild ships for nearly free according to their current position (and the market hasn’t moved).

- Their fleet utilization is reliably over 97%

- Their revenues for last year are 3.57X their MARKET CAP now.

- ONLY their total scheduled asset values of $488.9m is 20.80X GREATER than their current market capitalization.

- After–> DAILY OPEX; OWNERSHIP DAYS; FLEET OPEX; G&A EXPENSES; DEBT REPAYMENT; INTEREST EXPENSE; MAINTENANCE RESERVE, their break even point is slightly over $17,000. Anything above this is free cash flow and their fixing daily rates around $30,000 at near full capacity.

- The only trade able pure-play Aframax/LR tankers. Greatest operational trading flexibility among crude oil segments

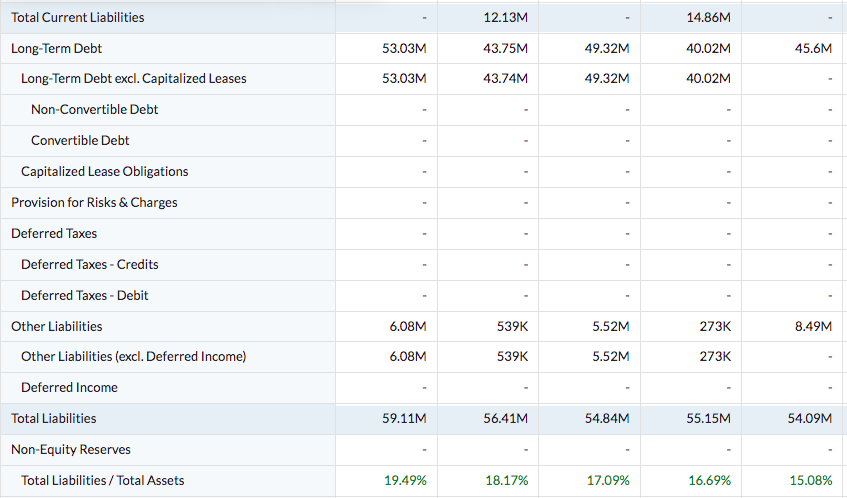

Balance Sheet/Performance

Really the only liabilities that are on the books are long-term

Revenue: $90m

Market Cap: $22m

Net income: $56m

Cash on hand: $68m (before bond raise; triple market cap)

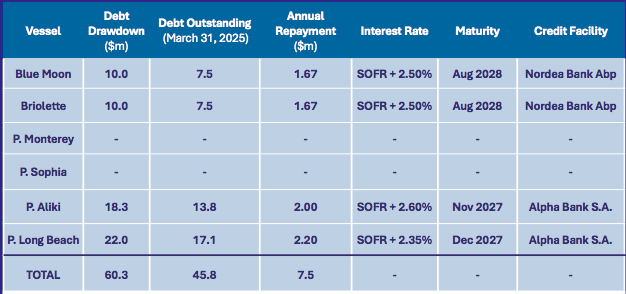

Debt

Their maturities on their existing debt doesn’t hold any maturity payments till late 2027. The payments are easily covered by revenue and cash (in fact the entire loans can be paid by revenues)

Highly skilled senior management team with strong industry and capital markets expertise

This isn’t a freak sort of performance either. Performance Shipping Inc’s trailing 12-month revenue (2023) is $108.9 million with a 52.3% profit margin, with prior years looking similar. What’s more is that their:

Voyage Expenses

Vessel Operating Expenses

Depreciation and Amortization of Deferred Charges

General & Administrative Expenses

they all have very high consistency from year to year (Time Charter Equivalent (TCE) rate $30,843 with

Daily Vessel Operating Expenses $7,173)

For the first quarter of 2025, they posted net income of $29.4 million and net income attributable to common stockholders of $29.0 million. This net income for the quarter is larger than their entire market capitalization of the company. These results are compared to a net income of $11.4 million and net income attributable to common stockholders of $11.0 million for the same period in 2024. Earnings per share, basic and diluted, for the first quarter of 2025 were $2.33 and $0.76, respectively.

Revenue was $21.3 million ($19.2 million net of voyage expenses) for the first quarter of 2025, compared to $22.4 million ($21.6 million net of voyage expenses) for the same period in 2024.

Performance Shipping has an ROCE of 21%, this result outpaces the average of 10% earned by companies in the industry. They are also employing 212% more capital than previously which is expected of a company trying to keep their fleet young and operatonal.

Growth

reported net income of $15.7 million and net income attributable to common stockholders of $4.6 million for the first quarter of 2023. Net income attributable to common stockholders for the three-month period ended March 31, 2023, has been adjusted by aggregate non-cash items of $10.6 million, as per US GAAP accounting standards, which do not affect the Company’s operating cash flows, EBITDA or performance overall. The 2023 first quarter results compared to a net loss of $2.1 million and net loss attributable to common stockholders of $11.5 million for the same period in 2022. Earnings per share, basic and diluted, for the first quarter of 2023 were $0.68 and $0.55, respectively, while loss per share for the first quarter of 2022 was $51.46

Expect More to Come

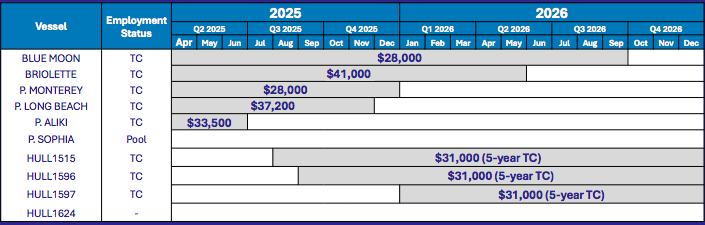

Currently, 9/10 of their fleet is under contract, despite only having 6 of them in the water so far. Their daily rate goes between $31,000 and $33,000 and you can see that at least 3 contracts extend beyond 2026 as the others conclude.

They currently have $220M revenue secured on backlog from 5 of their charters. They have existing relationships with some of the world’s largest companies including Chevron, BP, Glencore, Marathon and more.

Noteworthy News (last 3 years)

Sale of the two oldest Aframax tankers of the fleet for a gross sale price of $39.3 million, $44.8 million of voluntary debt prepayment and three new shipbuilding contracts

- the Company may repurchase up to US$2.0 million of its outstanding common shares, representing approximately 21% of the market capitalization of its outstanding common shares as of the close of trading on April 3, 2023; After this buyback programme they initiated another $2.0 Million dollar programme.

- December 13, 2023 – Today announced that, through a separate wholly-owned subsidiary, it has completed the previously announced sale of the 2007-built Aframax tanker vessel M/T P. Kikuma for US$39.3 million, with delivery of the vessel to her new owners

Also, later that year: through a separate wholly-owned subsidiary, it has entered into a time charter contract with Marathon Maritime Company (the “Charterer”), a wholly-owned subsidiary of Marathon Petroleum Corporation (NYSE: MPC), for the M/T P. Long Beach. The gross charter rate will be US$37,200 per day for a period of twenty-four (24) months +/- 40 days at the option of the Charterer and is expected to commence at the end of December. This charter will generate approximately US$25.7 million of gross revenue for the minimum duration of the charter. - May 2024: New Build–> through a separate wholly-owned subsidiary, it has signed a shipbuilding contract with Jiangsu Yangzijiang Shipbuilding Group Co., Ltd., Jiangsu New Yangzi Shipbuilding Co., Ltd., and Jiangsu Yangzi Xinfu Shipbuilding Co., Ltd., (collectively the “Seller”) for the construction of a scrubber fitted 75,000 DWT LR1 chemical/product oil tanker for a contract price of US$54.1 million excluding extras and net of commission to third parties. 15% of the purchase price is payable upon receipt

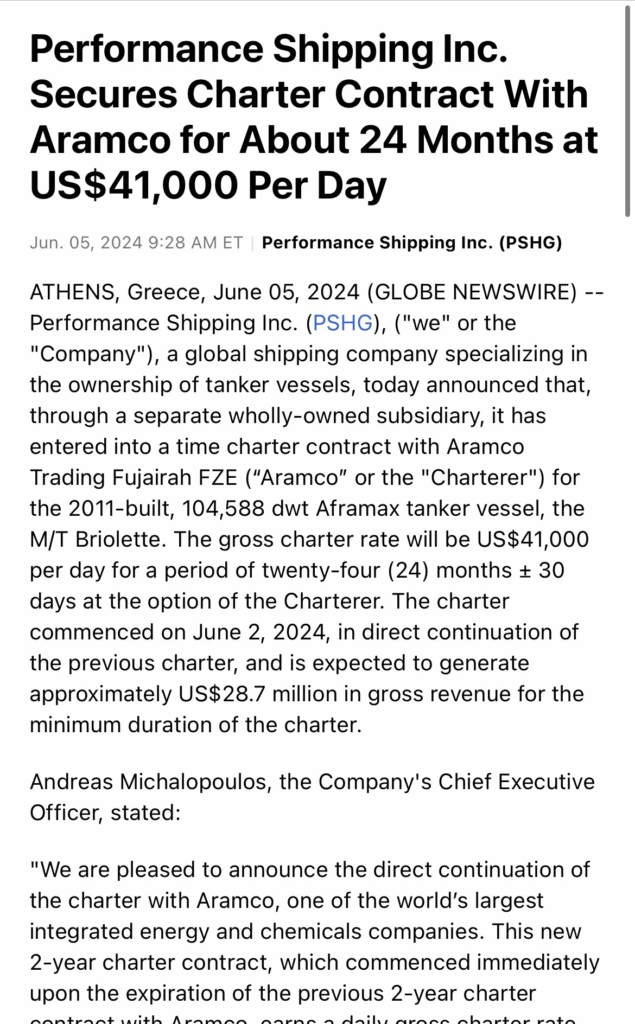

- June 2024: Performance has entered into a time charter contract with Aramco Trading Fujairah FZE (“Aramco” or the “Charterer”) for the 2011-built, 104,588 dwt Aframax tanker vessel, the M/T Briolette. The gross charter rate will be US$41,000 per day for a period of twenty-four (24) months ± 30 days at the option of the Charterer. The charter is expected to generate approximately US$28.7 million in gross revenue for the minimum duration of the charter.

- Dec 2024: Performance Shipping has secured a 7-month time charter contract with SeaRiver Maritime, an ExxonMobil subsidiary, for its LR2 Aframax tanker vessel M/T P. Aliki. The charter will generate approximately US$6.6 million in gross revenue at a rate of US$33,500 per day

- They have secured a 21-month time charter contract with American Eagle Tankers (AET) for its Aframax tanker vessel, M/T Blue Moon. The contract, starting in January, features a daily rate of $28,000, expected to generate approximately $17.4 million in gross revenue for the minimum charter duration (note how this compares to its market cap) (December 2024)

- January 2025–> Performance has extended the time charter contract with ST Shipping & Transport Pte Ltd., a wholly-owned subsidiary of Glencore for the 2011-built, 105,525 dwt Aframax tanker vessel, M/T P. Monterey. The gross charter rate will be US$28,000 per day for a period of twelve months +/- 30 days at the option of the Charterer. This charter will generate approximately US$9.38 million of gross revenue for the minimum duration of the charter.

- Through separate wholly-owned subsidiaries, it has entered into time charter contracts with Clearlake Shipping Pte Ltd (the “Charterer”) for the previously announced three new building LNG-ready, scrubber-fitted, LR2 Aframax tanker vessels. Each employment will be for a firm period of 5 years with the option to extend for a 6th and 7th year. The optional periods are to be declared by the Charterer 12 months in advance. The gross charter rate will be US$31,000 per vessel per day for the firm period of five (5) years, and a base rate plus profit share for the optional periods, if declared (March 2025)

- June 4th 2025–> A five-year USD denominated senior unsecured bond issue may follow, subject to inter alia market conditions. The net proceeds from the contemplated bond issue shall be applied towards fleet expansion and renewal and general corporate purposes of the Company

- July 24th 2025–> Through two separate wholly-owned subsidiaries of the Company. This facility refinances the full outstanding loan balance of US$29,750,000 previously secured by the M/T P. Long Beach and the M/T P. Aliki. This agreement follows the acceptance of a commitment letter from Alpha Bank, as previously announced on June 24, 2025. The Facility bears interest at the rate of SOFR plus 1.90% per annum and will be repayable in twenty (20) consecutive quarterly instalments of US$1,050,000 each, with a balloon payment of US$8,750,000 payable concurrent with the twentieth quarterly instalment in mid-2030.

- August 2025–> has entered into a time charter contract with Pakistan National Shipping Corporation (“PNSC” or the “Charterer”) for its M/T P. Aliki, a 105,304 DWT LR2 Aframax tanker, built in 2010. Under the agreement, the vessel will be chartered for a period of 12 months, plus or minus 15 days at the Charterer’s option, at a daily gross charter rate of US$30,000.

Ownership

Reports state that it is owned by 5.64% institutional shareholders, 0.00% Performance Shipping insiders, and 94.36% other investors, however, a recent SEC filing showed the CEO approximately 8.5% of the Issuer’s outstanding Common Shares. Acadian Asset Management LLC is the largest individual Performance Shipping shareholder, owning 459,092.00 shares representing 3.78% of the company.

Speaking of ownership, billionaire shipbuilder, CEO George Econmou has expressed interest in holding the whole lot. An exchange filing shows Economou holds an 8.8% stake based on the company’s 11.7m shares outstanding as of September 29, 2023; he now wishes to buy ALL outstanding shares for $3.00 per share (a 74% premium of current trading price). He sees value far beyond the 3.00 price if that’s his offer.

Bull

$3 Offer = 163% Premium: Sphinx (controlled by shipping magnate George Economou) is offering $3/share in cash. Even if you think Economou is the Gordon Gekko of Greek shipping, this is free upside if the deal closes.

2️⃣ Negative Enterprise Value: The company has more cash than debt. You’re basically getting tankers for free.

3️⃣ Insider Ownership: CEO Andreas Michalopoulos and Chairwoman Aliki Paliou control ~90% of voting rights. If they’re holding out for a higher bid, this could be a great shock to share price.

In their year end 2024 annual shareholder meeting they have produced a letter highlighting the company’s growth and strategic positioning with the following updates:

- The Company’s foundation for continued growth and value creation built on its unique pure-play Aframax tanker fleet, its simplified and transparent ownership structure and its significant management expertise.

- Performance’s execution of its focused strategy includes growing its fleet, leveraging strong relationships to secure commercial deployments at attractive rates, increasing sustainability and maintaining a strong financial position.

- The Company’s highly qualified and actively engaged board, the majority of whom are independent, is committed to acting in the best interests of the Company and all shareholders.

- The Board’s recommendation that shareholders reject George Economou’s goal of taking over the Company.

Their 192M total cash holding following a $100 million bond offering enables future acquisitions of companies or fleet and its strategic long-term partnership with a top-tier charterer. While some companies are in the mode of having to refinance at perhaps higher rates, they are cashed to the eye balls (FAR exceeding their market cap).

Commercially

They focus on short to medium-term charters with their already

▪ Established commercial relationships

▪ Presence in all major markets

▪ East and west of Suez Canal de-risking

They are regularly renewing their fleet in effort to reduce its average age.

Bear

Takeover Drama: Economou’s offer is highly conditional, and management is fighting it like the Titanic vs. an iceberg. Lawsuits, proxy battles, and a classified board structure are delaying everything. Given their low liquidity & lower volumes behind a small float, volatility goes up and down rapidly.

George Economou launched a takeover bid and tender offer for Performance Shipping in late 2023, believing the company’s shares were undervalued. The bid involved extending the offer deadline multiple times and facing legal battles with the company, which has described the offer as “illusory” and is defending against litigation intended to challenge its capital structure. Economou’s firm, Sphinx Investment Corp., continues to try and gain control of the tanker owner, extending the tender offer and engaging in proxy fights and legal actions against the company.

He has reaffirmed his offer to acquire the company by February 13th, 2026.

(+) there is a constant sense that investors have been left to dry with stock dilution and reverse splits (usually around a blowout earnings report or something)

Estimated daily cashflow

breakeven rates of approximately

$25,000–> makes them profitable, but deflationary pressures to rates can hurt margins

Shareholder dilution held down shares, which is no longer a major issue as they are now positioned very strong with a great balance sheet.

AI ask

To be honest, I had to ask AI why this stock was so crazily valued. These are the responses that it spit back to me–>The market is ignoring or heavily discounting recent earnings, perhaps treating them as non-sustainable or one-offs (this is not the case as they have been holding these numbers for a number of consequent quarters)

Or else there’s some risk that’s not immediately obvious: maybe concerns about future tanker rates, maintenance, vessel age, counter party risk, dilution risk (they might issue more shares), or corporate governance issues. (Okay, recessionary fears, but doesn’t explain the tiny valuations & there’s no visible mishaps from management)

Illiquidity and small float could lead to big discounts.

Also, potential takeover / tender offers might be involved (or rumors thereof) which could complicate the valuation. (Seems most likely the reason for the depressed prices)

Tariffs and warfare are a double-edge sword; on one hand it requires heightened demand for their oil/gas but on the other hand it runs the risk of blockade, seizures or burning fuel caught in canal blockades. Tariffs may also impact their ability to sign new, attractive contracts at a time when the existing ones run out.

A great meme… they are doing everything right, except helping our their share price… which could be a great buying opportunity for us to help them out!

Summing Up

I did find this company a couple years ago but given the shareholder dilution, talks of a takeover, and age of their ships–I didn’t bother looking into it further, despite the valuations being completely out of this world and it making money high margined cash flow. Now, most of those problems seem to have gone away and not only are they making money by signing large international contracts with fantastic day rates but they’re actively seeking to grow their fleet with new orders. If a shipping tycoon feels like paying a 160% premium for the entire company is worth it…what does he think it’s really worth?

Put simply, the valuations and trading prices compared to the net income, revenue and net value of the company are a joke. This is a company that could be trading +10X greater with ease–and I believe at some point you will see that level of return. We’re looking at a company holding a flawless balance sheet and undervalued during times of high debt and challenging competition in this capital intensive space.

They have:

- Cash (A LOT since their bond raise)

- Established commercial relationships & a commitment for fleet renewal

- Profitability

- A $220 Million Revenue Backlog, almost entirely paying for new builds, assuming no new revnues.

- Aligned Shareholders and Management (this is told by the fact that they didn’t sell for $3.00 a share; they both believe the company is worth much, much more.

- An enormous amount of catching up to do with their share price (relative to their enterprise value and earnings).

- Very little leverage

The threat of the Economou take over lurks still and it appears thats the number one reason why people are staying away, but the board has shown their resistance to giving in and control full rights over the terms of his offer [to be changed]. I believe that the valuation, fleet, cash holding, revenues, and continued deals will be too much for these insanely cheap valuations that investors cannot sensibly stay out. This will inevitably weaken the offer by Economou and hence make it less likely that he will be gain a fully takeover, at least…how he current wishes. Chances are he’ll be buying more shares with less voting power involved, which, is exactly what I am thinking on doing as well.

Thank you for reading–please share this amongst your friends and family!

#StayOnTheBall