Investment PowerPlay: An Interesting Silver Play Moving Quickly!

Before I continue, please give a follow of us on Soapbox here, Substack and view our other content on this site! There’s over 350 articles for your pleasure in Geopolitics, Finance, Travel and Stock Write-Ups!

Uniting two historic mines and unlocking their full potential for Broken Hill.

Company

Broken Hill, the entire ore body, is the single largest silver-lead-zinc ore body in world. As proof of this statistic, you have over 140 years of mining history and about 1 Billion ounces of silver pulled out from this region and 25 Million tonnes of zinc and lead.

A little history lesson here is that this deposit was founded by one man named Charles Rasp in 1883 seeking tin. He found no tin however and ownership changed hands to ultimately what would become BHP today, the Australian mining giant, who developed the silver property. Ever wonder what BHP stands for? The Broken Hill Proprietary Company.

History

Toho Zinc acquired the assets through their purchase of CBH Resources, and BHM subsequently acquired them from Toho.

Toho Zinc, a Japanese zinc producer, acquired the silver-lead-zinc resources by CBH Resources Limited, which held key mining assets throughout Broken Hill, Australia. The Endeavor and Rasp Mines, these assets, including the producing Rasp mine and the (then) mothballed Endeavor mine, had changed hands multiple times over the decades since BHP left the area in the 1940s.

In 2023–2024, Toho Zinc decided to exit its global mining business to focus on its core smelting business, initiating a staged closure of the Rasp mine and selling its holdings.

Broken Hill now owns 2 of the 3 operating companies that are now in this 28 kilometer stretch of the deposit.

Rasp Mine

The history of Broken Hill is intrinsically linked to the Rasp Mine. It currently operates as a silver-lead-zinc mine hosting a Mineral Resource Estimate of 10.1Mt at 9.4% ZnEq (5.7% Zn, 3.2% Pb and 49g/t Ag). The mineralisation is metamorphosed VMS (volcanic hosted massive sulphide). Some scary high grades tucked in there.

Our second ore body is now online, but its 2.5X the grade of the first ore body-Patrick Walter, CEO, MD

Western Mineralization deposit– operating for the last 12 years averages approximately 40 grams per tonne silver grade (placing is nearly as regarded as high-grade). This is their flagship area they are working on right now. The Western Min extends from approximately 100m below the surface to a depth of near 900m, where the deposit terminates against the Globe Vauxhall Shear. Mineralization identified below this structure is associated with the Centenary Deposit (below) which still remains open at depth

Features

Location: Centrally within the city of Broken Hill, New South Wales

Property Consolidated Mining Lease 7 (CML 7) inc. Mining Purpose Leases 183, 184, 185, 186, as well as ML1249, EL5818 and EL6059.

Mining Method: Sub-level open stoping and up-hole stoping

Processing Method: Grinding, flotation, thickening and filtration

Mining this was still attractive when the silver price sat around $26 USD per troy ounce!

Main Lode, the new ore body is placing a reliable 150g/t silver. It’s worth mentioning that development of this location was profitable enough for the company when silver was 25 USD per ounce (now look at silver). Some looks at these grades are as follows:

Blackwoods: 490kt @ 18.3% ZnEq (8.3% Zn, 7.5% Pb & 156g/t Ag)

British: 180kt @ 15.5% ZnEq (7.2% Zn, 7.2% Pb & 101 g/t Ag)

NBP: 140kt @ 21.6% ZnEq (8.3% Zn, 9.4% Pb & 222 g/t Ag)

Wilson: 60kt @ 11.1% ZnEq (5.6% Zn, 3.9% Pb & 105 g/t Ag

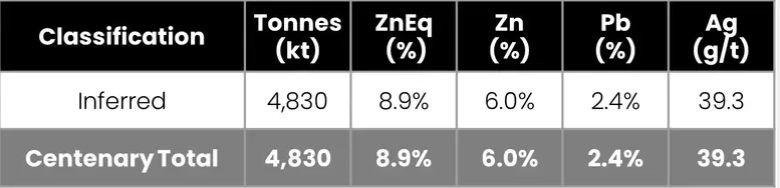

Last is Centenary. A deposit that remains completely unmined to date

Limited exploration drilling (13 holes), orebody requires more drilling & definition (open in all directions). This is pure speculation and potential increases to the company’s NPV later on, but nothing to bet the farm on.

Expected upside in grade and tonnage as orebody knowledge improves

Exploration plan to use lower levels of Western Min to establish drill platforms

Given the depth of this finding, we likely won’t hear more about it for a little time.

You’ll find other findings within their published Mineral Resource Estimate here: https://brokenhillmines.com/local/documents/RASP-MRE.pdf

Second Mine, Williams Family

This area is considered to be one of the highest grade and shallowest deposits in Broken Hill, the Pinnacles Mine remains relatively undeveloped, with only small-scale historical mining targeting whats called the rich Galena (lead ore) lodes

Mineral Resources 6.0 million tonnes @ 10.9% ZnEq (4.7% Zn, 3.3% Pb & 132g/t Ag)

Exploration Target 6.0 – 15.0 million tonnes @ 2.0 – 4.0% Zn, 3.0 – 6.0% Pb, 40 – 125g/t Ag

Its current transportation method (proposed) is via existing haul road and public roads to Rasp site. It currently sits approximately 15KM outside of the nearest town.

Interestingly, this was acquired by a family who were privately mining this area for 75 straight years. Only involving the family, they’ve built a 50 meter open pit mine and an underground shift extending down to 75 meters. They even built their own processing plant and given the high grades, they had no need for official assays. They all did this without engineers, consultants, teams, external professionals, etc. ALL of this drilling had been private till today–a 1900’s mine in hiding essentially!

Missed Chance Back Then

Furthermore, Planned Pinnacles IPO was scheduled to occur in 2007, but was ultimately stopped due to the global financial crisis. In this time, The Williams family had continued to define further potential of Pinnacles over the last 15

years.

Similar to the stock write up I’ve done below by clicking the button… I enjoy stories like this behind the investment thesis. In this instance, this is a unique property that begins to set the mining company apart because at the end of the day, there’s thousands of these companies all telling you that they’re the next big thing on the block.

Upon completion of drilling, BHM will immediately start a Mining Expansion Study to assess the incorporation of Pinnacles ore into the Rasp Processing Plant. Take a look at some of the findings to date…

- 8.9m @ 54.6% ZnEq, 1,537g/t AgEq (922g/t Ag, 12.3% Pb, 1.6% Zn, 3.7g/t Au) from 11m PN311

- 8.2m @ 40.4% ZnEq, 1,120g/t AgEq (763g/t Ag, 13.4% Pb, 1.7% Zn, 0.4g/t Au) from 18m PN310

- 4.0m @ 29.8% ZnEq, 827g/t AgEq (536g/t Ag, 9.9% Pb, 2.0% Zn, 0.3g/t Au) from 60m PN302C

- 11.8m @ 25.2% ZnEq, 698g/t AgEq (476g/t Ag, 7.4% Pb, 0.7% Zn, 0.06% Cu, 0.6g/t Au) from 3m PN314

- 5.7m @ 24.0% ZnEq, 663g/t AgEq (52g/t Ag, 1.4% Pb, 16.4% Zn, 0.13% Cu, 1.4g/t Au) from 17.3m PN313-A

- 19.4m @ 23.7% ZnEq, 657g/t AgEq (443g/t Ag, 8.3% Pb, 0.7% Zn, 0.3g/t Au) from 95m PN306

- 6.0m @ 23.3% ZnEq, 644g/t AgEq (68g/t Ag, 1.9% Pb, 15.7% Zn, 0.11% Cu, 1.1g/t Au) from 16m PN313

- 5.2m @ 16.6% ZnEq, 459g/t AgEq (278g/t Ag, 5.4% Pb, 1.6% Zn, 0.3g/t Au) from 200m PN325C

- 12.0m @ 14.5% ZnEq, 400g/t AgEq (36g/t Ag, 0.7% Pb, 10.0% Zn, 0.10% Cu, 0.8g/t Au) from 233m PN325

- 10.9m @ 13.3% ZnEq, 366g/t AgEq (29g/t Ag, 0.7% Pb, 9.0% Zn, 0.13% Cu, 0.8g/t Au) from 21m PN314

Management believes that this mining property is positioned to be the largest discovery in the Broken Hill deposit in the last 100 years. Thus far, they’ve been able to reliably find grades of silver that are north of 150g/t. An open-pit mining decision will happen in Q2 2026

Functional Company

Broken Hill also has a 750,000 tonne processing plant in their possession (processing silver-lead-zinc), a major upgrade from when the plant was acquired, about 200% less productive than it is today. A single stage jaw crusher and two stage grinding circuit are used to liberate the valuable minerals from the waste rock. These minerals are then separated from the waste using the traditional, sequential flotation process.

Stats since 2013:

- Zinc recovery (avg.): 88%

- Lead recovery (avg.): 88%

- Silver recovery (into Pb conc., avg.): 75%

- Zinc concentrate typical grade: 49-50% zinc

- Lead concentrate typical grade: 65% Pb & 800 – 1,000g/t Ag

Mining techniques employed at Rasp Mine include longhole open stoping, modified avoca, cut-and-fill and room-and-pillar. Approximately 60 stopes are extracted per annum with mining depth at approximately 500 metres below the surface.

Other Infrastructure includes an operating plant, sealed road and rail services, grid power to mine (22kV transmission)

Crucially, the workforce is residential able to live nearby. Currently they have 118 employees & contractors.

Logistics

Two concentrates are produced – a lead-silver concentrate and a zinc concentrate. Tailings from the process are placed in the surface tailing storage facilities in the Blackwood’s Pit (TSF 2) and the Kintore Pit (TSF3).

The concentrates are thickened and then filtered. The filtered concentrate is discharged directly into sealed concentrate containers which are then trucked less than a kilometer to the Rasp rail siding. The lead concentrate is railed directly to the Port Pirie smelter (or can also be exported) and the zinc concentrate railed to the Port of Adelaide where it is unloaded and ultimately shipped to smelter facilities globally.

In-house team

Mining operations are undertaken predominantly by an owner/operator workforce, with contractors being utilized to undertake only specialized support services like diamond drilling.

Did You Know?

I am building a platform for intellectual content with a free-speech agenda supporting it? It will become a place where stock picks and write-ups will be found for you as a reader! Allow me to introduce you to Soapbox.

Visit www.writesoapbox.com

Numbers

Assets

Current Assets

- Cash & Cash Equivalents: A$2.36M

- Trade & Other Receivables: A$15.64M

- Inventories: A$8.18M

- Other Current Assets: A$0.99M

➡️ Total Current Assets: A$27.17M

Non-Current Assets

- Property, Plant & Equipment: A$15.84M

- Exploration / Evaluation / Development Assets: A$28.99M (Rasp & others)

- Other Non-Current Assets: A$3.41M

- Right-of-Use Assets: A$4.80M

➡️ Total Non-Current Assets: A$53.04M

Total Assets: A$80.20M

Liabilities

Current Liabilities

- Trade & Other Payables: A$26.57M

- Lease Liabilities (Current): A$0.60M

- Contract (Deferred) / Unearned Revenue: A$15.21M

- Employee Benefits – Current: A$2.39M

- Convertible Notes / Short-Term Debt: A$9.20M

➡️ Total Current Liabilities: A$53.97M (Their current liabilities are exceeding current assets... indicating that they may have to do another capital raise and/or roll over their existing debts).

Non-Current Liabilities

- Lease Liabilities (Non-Current): A$4.24M

- Employee Benefits – Non-Current: A$2.68M

- Environmental Rehabilitation Provisions: A$15.88M

➡️ Total Non-Current Liabilities: A$22.79M

Total Liabilities: A$76.76M (please note their total assets in excess)

PLEASE NOTE: these numbers are the official numbers last filed in June 2025… but they’re looking much better after two capital raises:

Market Cap 195M market cap now

73M AUD is in cash.

38.1 AUD is in debt

Recent Capital Raise has 48% going to drilling and approx 30% going to revamping their processing plant.

Rasp Expanded Drilling Program (17,000m)AUD 7.8MPinnacles Exploration Expansion (25,000m) AUD 11.0M

Latest Presentation

Experienced Team in the Region

Interesting Big Picture

- Silver, that many are now bullish on for all sorts of reasons (industry demand, monetary allure, supply issues) is mostly mined as a result of lead and zinc mining as a byproduct.

- Not many silver companies listed on the ASX

- Share prices have yet to catch up with their explosive exponential margins, despite fantastic performance for shareholders over the last year

- Raised 20M AUD at 35 cents; months later, raised 38.5M at 1 dollar price AUD. Demand is there from investors.

- Very young company, not many people know about them.

- In an extremely mineral rich area almost by sheer luck.

Current mining operations are primarily focused on the extraction of the Western Mineralisation (WM) and the original Main Lode mineralisation

Closing

What we are looking at here is a very high grade pure silver play, that very few know about (perhaps due to the involvement of the private family ownership or the recent incorporation), with exploration upside, their own processing capacity and logistics intact already. It’s worth reiterating that the Broken Hill deposit is the largest known silver-lead-zinc deposit in the world, exactly where this company, with a relatively small US-equivalent of 130M market cap, is operating. Moreover, most of their project areas have yet to be fully explored to get a sense of the scale of their ounces in the ground.

Not only are they dealing with a deposit that previously was a mining behemoth, but they still believe can produce for another 100 years. This had seemingly been lucked into acquiring it due to a corporate decision from Toho Zinc, peanuts on the dollar if you will. Further drilling leading into production is made possible with their relatively healthy balance sheet and ability to raise capital confidently.

As silver enters its 6th consecutive year of deficit, the world is going to be scrambling for any silver, anywhere (this is why we’re seeing an Asian silver arbitrage play between Tokyo and Western markets). This company, I suspect, is going to be a major provider of that silver operating on stupid high net margins. This one is definitely worth considering for your portfolio!