Investment Powerplay: South American Project Generator

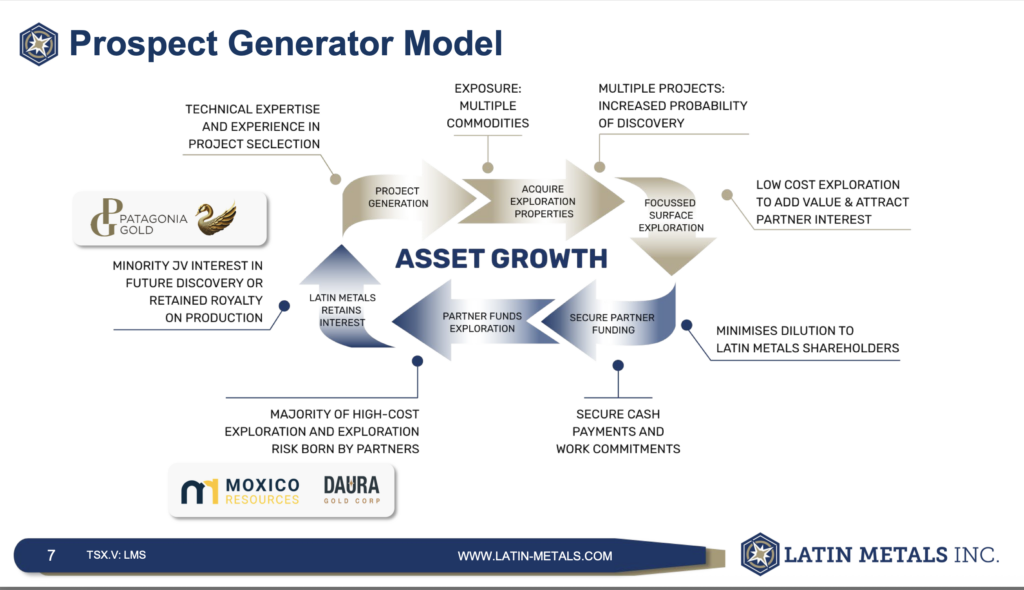

Latin Metals is redefining the junior mining model through a pure prospect generator strategy focused on Argentina and Peru. Interestingly, unlike other project generators, they’ve abstained from running costly drilling programs. The company identifies and acquires prospective mineral assets following staking the property, then partners with well-capitalized operators who earn majority stakes – typically 70–75% – by completing drilling programs themselves.

This approach allows Latin Metals to operate on a lean $2–3 million annually while avoiding shareholder dilution, which is so common in this mineral resource space.

Currently, the company has secured approximately $80 million in partner-funded exploration, with expectations to grow this to $160–180 million as additional projects are optioned. What a model, let someone else do the spending!

Speaking of spending, if you appreciate this research and obscure equity-write-ups, for only a little more than $5.00 a month you have access to ALL of my investment content material.

We don’t. We don’t operate. We would if we had to but…never. That’s the rule. -Keith Henderson, CEO

A key innovation in its model is structuring earn-in agreements based on drilling meters instead of expenditure commitments. This is because a big large company can easily piss away money on their corporate headquarters to hit their targets in the contract–whereas what matters for Latin Metals are meters drilled in the ground to expand the property.

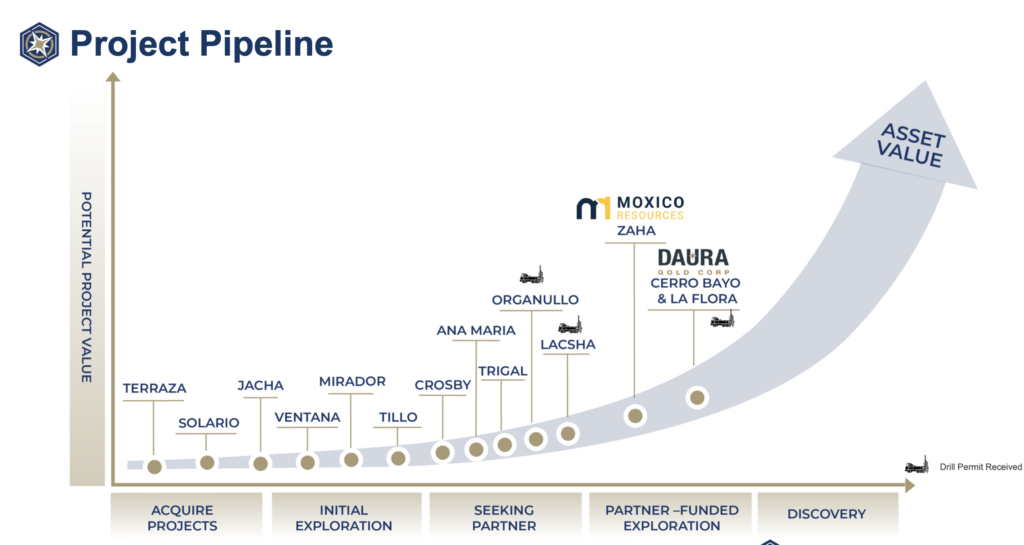

Latin Metals’ portfolio is only in Argentina and Peru but they have expressed interest in Chile and an antagonism towards Ecuador. Their products include a 500,000-hectare land position in northwest Argentina prospective for sediment-hosted gold deposits. This extensive land package provides significant scale and positions the Company as an early entrant in a largely under-explored belt. This is the preliminary investigations, again, crucially, not drilling, to evaluate whether there is the potential for a system here for others to explore. (half a million hectares is a giant land package!).

Its partnerships include major and mid-tier players such as Moxico Resources, alongside past or ongoing relationships with Newmont, Barrick, and AngloGold Ashanti. The company’s long-term strategy is to evolve into an organic royalty business.

As you can see from their project pipeline, this is what makes this model so unattractive to investors (yes, you read that correctly)–it’s slow and most of the time nothing happens because the bulk of activity early on is acquiring projects, doing some brief exploration with some partners who may be flaky, but this is where I sense there is an advantage.

In other words, I believe we as investors have an edge in being early at a price that is more attractive than it otherwise would or should be; since investors may be looking at this with very little excitement over the next 6-12 months.

The upside is fully realized once a discovery is made and it can be converted into a cash flowing property where they will retain rights to this revenue [in the form of royalties].

My other investment business heavily focuses on these types of long-term, patient investing opportunities as approaches to preserve wealth and patiently let the value creation occur- Sea Lion Investment Office

News (Latest Deals)

Latin Metals Inc. (TSXV: LMS and OTCQB: LMSQF) reports that it has received a US$250,000 cash payment from Daura Gold Corp. (“Daura”) consisting of US$150,000 payable to the underlying vendor (“Underlying Vendor”) of the Cerro Bayo and La Flora properties (the “Projects”) and US$100,000 payable to the Company.

Under the terms of the option agreement, Daura may earn up to a 75% interest in the projects (80% with a top-up right) by completing staged exploration, including aggregate payments of US$1,700,000 (US$300,000 paid), aggregate payments of US$400,000 to the Underlying Vendor (US$250,000 paid), complete exploration work commitments including 28,000 metres of drilling (1,850 metres completed thus far).

Around 40% with Management and Board having ownership of the shares

So what this translates to, are cycles of receiving cash payments for the purposes of exploration of their property, while holding a retained 20-25% of whatever they find (and crucially all of the data if the deal completely falls out of favor). They are able to inch the needle a long, survive another day if you will, to utilize their geologically expertise to acquire more mineral rights and scope geological projects worth pitching for future partnerships.

Furthermore, by retaining net smelter return (NSR) royalties and minority stakes, Latin Metals gains exposure to future production and rising commodity prices without assuming development costs. Additional value is realized through staged cash payments tied to resource estimates. With improving mining sentiment politically in Argentina and strong demand for advanced projects from the majors, Latin Metals is positioned to benefit from multiple near-term exploration catalysts for a re-rate. Its disciplined and patience, but a capital-light model offering diversified upside while maintaining exposure to the commodity bull market and minimizing risk.

Ultimately, Latin Metals have the attitude, you do the work, we profit–and we’re happy to wait

A last thing I like about Latin Metals is the potential spin outs that can occur as an investor. Ultimately, they don’t have the income and therefore the cashflow to justify dividends or even share buy backs in a significant way. Instead, because they have so many projects that they issue to others, if there is a significant hit that becomes a separately company worth economically mining the deposit for the long term, we as shareholders may be granted a percentage of shares in a new company by holding Latin Metals.

It may be unexciting for your average trader–but for a long term investor, it ultimately means your own assets and portfolio grows with time.

Closing

On The Ball is a newsletter and blogging subscription that seeks to view the big picture and apply it to stock picking and wealth preservation. This purpose, with Latin metals, speaks to a very patient, far-sighted investor who is willing to wait for the upside opportunity to take place all while experiencing minimal downside risk.

Most finance media companies won’t write about these stocks because they don’t sell flashy headlines to sell to readers “ha-ha I told you so!”. But this mixes the big picture of where matters are trending.

In the event of

- Gold and silver continue to rise in price

- Argentina mining continues to be favored

- Major big finds become rarer

- Drilling is increasingly permitted from governments around the world [because of the energy and critical mineral crisis]

- This company adheres to their no-drill policy, accumulate royalty agreements and expands their portfolio into Chile

This company is positioned very well in the future. It may be a cliché to say, but all it takes is one major deposit to be explored paying a 2-3% NSR (net smelter royalty) for this company to become an ATM, and lucky for them, they have projects progressing a long the way.

#StayOnTheBall

https://substack.com/@ontheball1

https://writesoapbox.com/profile-page/1732776153389×907555635913884300 I’m on Soapbox!