A Gold Producer With a Monthly Dividend?

Yes, you read the title correctly. This is what first turned my head onto this company as well. Gold lovers will enjoy reading about this one if they haven’t heard of it before

Projects

Golden Mile

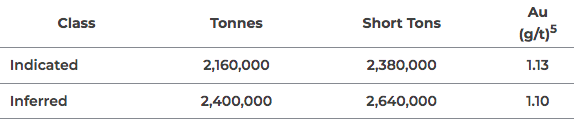

Millions of ounces of average grade gold.

County Line is expected to become the transition focus from Isabella Pearl.

The Company owns 100% interest in the County Line property, located in central Nevada’s Walker Lane Mineral Belt in Mineral and Nye counties. The total land package is 2,400 acres consisting of 116 unpatented lode mining claims and 6 unpatented placer mining claims. The property is located within close proximity, approximately 14 miles northeast, of the Company’s Isabella Pearl Project

The County Line property is part of the Paradise Peak collection cluster of high sulfidation epithermal deposits. The district historically produced a total of 1.5 million ounces of gold and 38.9 million ounces of silver. The County Line open pit historically produced approximately 81,000 ounces of gold and 760,000 ounces silver. The Porphyry (East) Pit, located approximately 2,500 feet southeast of the County Line pit, produced approximately 7,400 ounces of gold and 8,000 ounces silver. While both open pits represent exploration targets, other targets include “Newman Ridge” and the “Jackpot Zone”.

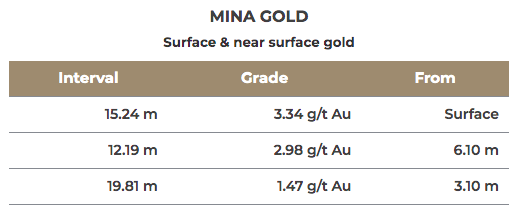

Mina Gold

Fortitude Gold owns 100% interest in the Mina Gold property located in Nevada’s Walker Lane Mineral Belt. The property has the potential to be a future open pit heap leach gold operation. Mina Gold reported a historic third-party estimate of mineralized material totaling 1,606,000 tonnes grading 1.88 g/t gold. The property covers an area of approximately 1,200 acres consisting of 61 unpatented claims and 5 patented claims.

East Camp Douglas

Prior exploration by several mining and exploration companies has established modest gold resource potential in five separate areas on the property, with over 3,000 meters of drill core and a large exploration database. The Company believes this large property has numerous untested gold targets with open pit heap leach potential warranting an extensive exploration program.

Here there is huge potential upside with respect to Fortitude’s balance sheet as this asset only had come up with gold in five areas with only 3K meters completed thus far.

Like the other deposits, at or near surface

On Sale?

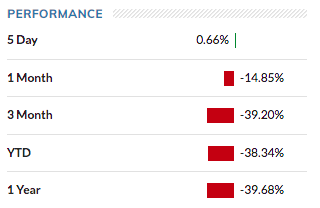

Recent Performance

Revenue Hits $6.5 Million for Q1 2025

Gross Profit of $3.3 Million for Q1 2025

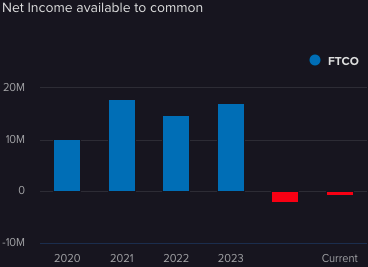

Net Income $1.2 Million for Q1 2025

EPS: 0.05

The 2024 year showed a pullback in both income and expenses to a great degree, and some shareholders have been spooked.

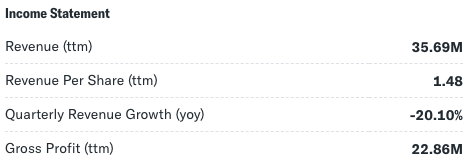

For this off year (2024), they showed achieving $37.3 million in revenue and $1.4 million in pretax income. The company produced 16,472 gold ounces and maintained a total all-in sustaining cost of $966 per gold ounce.

The company faced exploration expenses amounting to $1.4 million and distributed $2.9 million in cash dividends to shareholders. The cash balance as of March 31, 2025, stood at $21.4 million, with a working capital of $30.7 million.

| Revenue 35.689M so far this year 2025 |

Have to Talk About Dividends

I have been watching this company for awhile trade around 4-6 dollars up and down while paying a dividend ranging from 7-13%, monthly. Before the recent pull back, the company was paying a 14.80% dividend. If you search Fortitude gold on YouTube you’ll be hit with numerous titles of “gold producer paying dividends and no debt!” or some variation of it. They’ve kept their goals steady for the last 5 years (as far as I can tell).

For Q1 2025, they accounted for $2.9 million in cash dividends to shareholders which was double that of exploration expenses and about an eighth of current cash holdings.

Right now, at 12 cents a year they’re plugging the lowest dividend they have in years at 3.3%

History

This leads me into explaining a little more of the history of the Founder and what he has done before.

GORO was designed with a tight capital structure ensuring that they were capable of paying a dividend–they want to replicate what they’ve done with that company with Fortitude.

While at Gold Resource, the current CEO of Fortitude generated over 1B dollars of revenue (across about 10 years), returned 116M to shareholders and remained profitable throughout the entire time (including major bear markets).

Their trick is that they’ve acquired high grade open-pit mines during the bear market

My head first turned when I see how they were cashing up their balance sheet to pay dividends from their near-surface gold with excellent margins (with such low AISC) in a Tier-1 jurisdiction.

Ratios

P/E: Normally around 8-9, currently negative due to negative earnings.

P/B: 0.81

P/S: 2.44

Beta 0.46

Current Ratio: 9.83

Quick Ratio: 7.25

Cash Ratio: 6.81

Balance Sheet

Cash (Q1 2025)–> $21.4M USD

Net Debt–> -23.68M

or Debt-free.

125.34M –>Total Assets

5 year average 124.74M –> indicating a steady operating procedure by management (as I said, the management's goals haven't changed much)

Dividend Pullback & Share Collapse

In their 2024 report they have announced: The Isabella Pearl project (main producing project) is expected to conclude mining operations in the first half of 2025, with an estimated 43,000 recoverable gold ounces remaining on the heap leach pad. The company is evaluating a potential pit wall layback and awaits permits for its next mining operations, including the County Line project.

Upon news of permitting delays for its County Line Project there has been a strategic 75% pullback in the dividend from 4 cents back down to 1 cent which caused the stock price to fall considerably.

However, I believe this is a temporarily setback at a time when investors are genuinely conservative on where to allocate. In the meantime, the dividends will continue if not rise back again and we have a chance to pick it up at cheaper valuations for those who believe the thesis of returning value to shareholders.

The reality is a fall was always going to take place. They were going to run out of mining in Isabella Pearl 2 years prior but they found other ounces beneath them which had extended their mine left. Their ore turns into a sulfide which they cannot extract with their existing heap leach methods (they’re looking for open-pit, oxide ore).

Downsides

- The ability to continue mining their existing resources is expected to come to a close halfway through 2026; one can expect higher CapEx and mining risk beyond

- They are dependent on permits to resume operations at their other deposit

- No 2025 production guidance provided at the end of FY2024 with a smaller exploration budget

- Difficulty acquiring substantial institutional capital given their slow-and-steady (low growth) operations.

Slowdown

Fortitude does look like it’s experiencing a slowdown in many metrics aside from their gold mine coming to an end.

Capital Expenditures Growth Rate 5Y (TTM)-31.24%

Total Revenue Growth Rate 3Y (TTM) -23.1%

Permits are not entirely needed for County Line due to its proximity to former Isabella Pearl before going to Golden Mile

The reduction (from 40,000 to 16,000 ounces of gold) had been predicted, I expect them to ramp up production once again soon and continue to find surface-level finds with their other properties.

What Makes This Investment Unique

- Direct gold price exposure; margins can explode.

- Continued dividend payer despite the market problems, slowdown in operations and drill delays; A history of being the gold-dividend payer with prior companies and intend to do the same with Fortitude.

- Their near surface-level approach means that their assets are able to be sold off when they no longer have use for it themselves.

- Other resources to explore to continue mining operations; they don’t have the added expense given the proximity of their next mining asset (they’ll haul it for processing). They aim for 10-12M USD a year allocation to continue to widen their operation in terms of size and life of mine.

- Conservative, predictive balance sheet at all times

- Aiming for 40-50,000 ounces of gold produced her year, profitably for shareholders. Staying in their zone (not trying to find the biggest deposit and burn cash doing so).

- Tier-1 jurisdiction

- 2024, a bad year, still produced an AISC of $966/oz

- Hardly any institutions are involved; potential share appreciation

Disclaimer

Throughout Investment PowerPlay I have a number of stocks that could be explosion given the correct theme or thesis coming true; Fortitude Gold Corp, I don’t believe is one of these. This stock is similar to this one I wrote about:

Closing

Fortitude Gold Corp is a unique way to play the rise in gold price. I like this company as it’s now being traded for bargain prices after a predicted fall, with lots of mine left ahead of it, while it pays dividends due to its low AISC and management philosophy. Hedging out downsides and playing it safe, I think this company is an interesting play for most portfolios–> it won’t be explosive like the exploration miners but you’re not risking an 80% downside neither.

If you want to hear more stock write ups, chat to me personally, or learn about the business activity I am investing in/working on–consider joining as an On The Ball member!