*Non-Subscribers Temporary Access*

A French Company To Look At Despite Europe Crumbling

Mersen SA, formerly Le Carbone Lorraine SA, is a France-based company engaged in the production of carbon and graphite products and its application in an array of industries. The Company’s activities are divided into two sectors: advanced materials and electrical power. The advanced materials sector includes graphite anticorrosion equipment, brushes and brush holders for industrial electric motors, and high-temperature applications of isostatic graphite. The electrical power sector includes solutions for energy management (namely power electronics; supplier of passive components for power electronics), electric protection (renewable energy) and monitoring in industrial fuses manufacturing and current collection for the rail market.

Mersen now has a footprint in over 50 countries around the world.

Stock

Current Price: $21.55 and holds an estimated Year 2025 Target: $50

Market Cap: 523.36M EUROs

Shares Outstanding (million): 24.36

7.47M Employees.

MRN.France // 0Q6Q.UK // CBE.Germany // CBLNY.USA

Sectors

To be honest, I began writing out all of their sectors but realized I was simply burning time so here is a link to see for yourself–it’s a lot!

https://www.mersen.com/en/all-markets

The main takeaway is that their exposure to nearly every industry creates a situation where they are far more resilient than other industries. It doesn’t matter what happens in the world, whether we go green, go to war, innovate with data centres, go “dirty” mining or stick to the basic materials (rubber, glass, oil, plastic, cement)–Mersen will be involved since they’re behind these megatrends.

Ratios

Market Cap: 597.3M USD.

Revenue/Shares: 53.36

Price/Tangible Book: 1.80

EPS : €3.42

EPS Growth: 13.30%

Return on Equity: 10.90%

Quick Ratio: 0.56

Altman Z-Score: 2.64

P/Cash flow per share: 6.35 (Industry average is 0.44)

Beta: 1.88

I have written extensively on how much trouble that Europe (particularly the EU) is in for the foreseeable future; even if the macros aren’t aligned, this is an interesting company

Performance

| Gross Margin % | 31.02 |

| Operating Margin % | 10.54 |

| Net Margin % | 4.74 |

| EBITDA Margin % | 14.19 |

| FCF Margin % | -1.82 |

| ROE % | 7.22 |

| ROA % | 5.4 (Interesting this is what it was at the 2020 crash) |

| ROIC % | 6.95 |

Of Mersen’s 1.2 Billion for revenue in 2023, $310M originated from Asia, and $463 from the North America, it’s largest market. It is a beneficiary from further electrification efforts. The Euro strengthened their reserves while they were still growing (not losing sales).

In 2024,

- Record sales of €1,244 million

- Excellent operating cash flow before capital expenditure, above the 2023 level

- Net income attributable to Mersen shareholders of €59m

- Solid financial structure: Net debt and leverage at 1.8x, better than expected

- Proposed 2024 dividend of €0.90 per share, in line with the Group’s distribution policy

- 2025 guidance:

- Reported sales to remain stable or increase compared with 2024

- EBITDA margin before non-recurring items of between 16% and 16.5% of sales

Q1 2025/4

This first quarter has been worse, but it was expected given Trumps tariff talks + Chinese economy contractions. wind, rail and aeronautics markets gained attention. Asia-Pacific has contracted a considerable amount from weak demand for solar panels out of China but India has softened this fall due to its rising demand for Mersen’s products.

If we look more recent, first-quarter sales of €305 million, -6.4% on an organic basis and -2.5% on a reported basis. Group sales are up on an organic basis, excluding solar and SiC semiconductor markets. This would put their 2025 performance close to 2024.

Story

This company has also not seen wild speculation and outrageous growth predictions given the semi-conductor craze both in 2021 and 2024 either. Their operating accounts are the primary sources of it’s financing. Some may be missing this stock as it may be contrary to many right now given the fact that it is an industrial sector play.

While they play a conservative balance sheet, Mersen has the ideological backdoor option to grift by issuing green bonds, too. If the ESG monkeys or perhaps the CBDC investors who are forced to invest in “environmentally friendly stocks” roll in, maybe this could benefit a lot from these Euro funds.

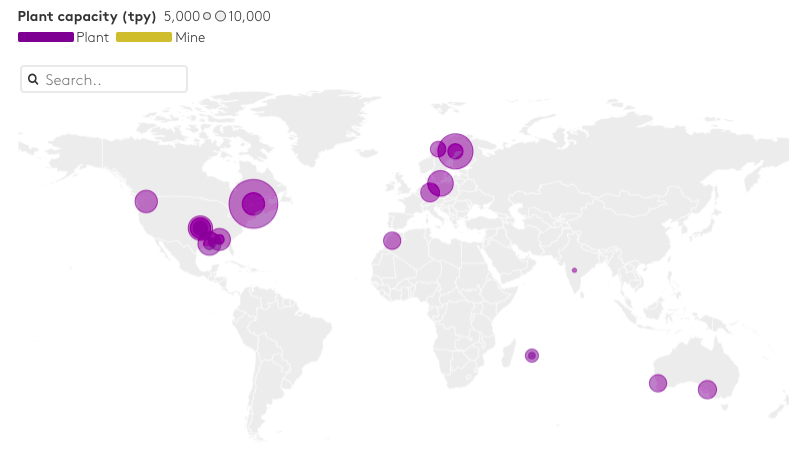

Graphite & Silicon Supply Chain?

All of the places where there are mines AND plants to process the graphite are in what you’d call “Western-friendly” nations. See the yellow dots

This ensures that Mersen’s own supplies will more than likely be secured into the future.

But Not too European

Only about 20-30% of Mersen’s revenue comes from France with around 50% from outside Europe altogether (notably Asia and North America). So even if France or the EU slows down, Mersen still benefits from booming industrial investment in the US (especially chips and EVs) [and Asia too, although I’m reluctant to be too bullish on Asia].

Balance Sheet

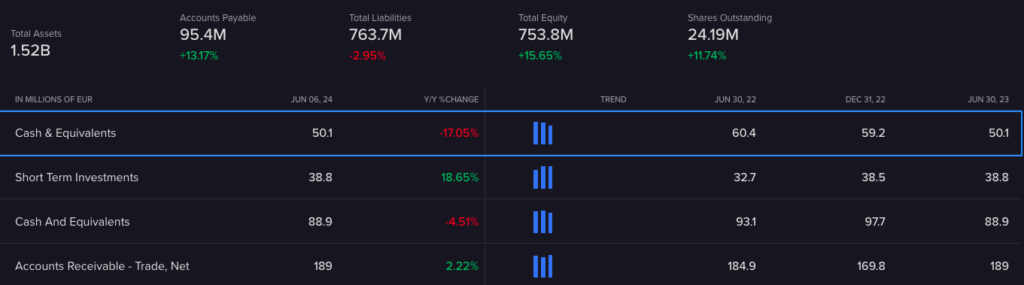

Their balance sheet is solid with many assets and accounts receivable double that of their accounts payable. They have been gradually paying down their current liabilities over the last 3 fiscal quarters. They hold about 51.3M (Euro) in cash and equivalents

Net Debt (total gross debt minus cash & equivalents): €370.3 million

Total Assets: €1,801.4 million

Total Liabilities: €919.0 million

Total Liabilities/Total Assets: ~50%

Total Current Assets: €590.4 million

Total Current Liabilities: €427.4 million

Current Ratio (Current Assets ÷ Current Liabilities) –>1.38

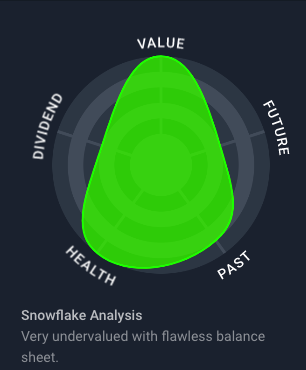

Valuation

- Trading at 52% below our estimate of its fair value

- Earnings are forecast to grow 12.27% per year

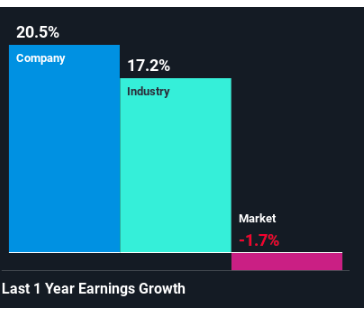

- Earnings grew by 20.5% over the past year

Trading at a good value compared to its peers as well, with analysts in agreement it is very undervalued

Mersen holds a 3-year- payout ratio of 35% (retaining 65%).

The company has been profitable 9 out of the last 10 years with a top-notch moat score.

Stickiness

Mersen is a company that has been incorporated since 1937, meaning they have decades of know-how in specialty graphite and materials science.

The main matter, relating to their moat in this industry however is that since their clientele are so diverse, they must offer tailor-made solutions and long sales cycles – These customers require high-certification, which makes switching away from Mersen difficult, time consuming and they can’t afford to shop around for other producers.

Mersen is also in an industry where supplies offer mission-critical applications (e.g., semiconductors, nuclear, rail, military) where failure is not tolerated. This cannot be said for other stocks relating to fintech.

Ownership

Ownership is roughly split between the general public and institutions (who hold 58% of total equity). Only about 1-2% of shares are held by insiders, but they have shown a 13% increase in buying their own stock (340K) in 2023 and little chance since.

Mersen is often #1 or #2 globally in:

- Graphite for semiconductors and high-temperature applications.

- Electrical protection for industrial applications.

- Busbars and cooling systems for EV powertrains and converters.

Growth

Their financing over the last 5 quarters has been pretty steady and not diving into debt too fast.

The last year posted a net income growth of 5.53% despite negative cash flows (one-time due to capital expenditures?) and a new level of debt of 2.3x EBITDA.

Dividend

They’ve kept their dividend going since 2019 notwithstanding a pretty significant cut in 2021 by paying those on record as of July every year. The dividend of 2024 is the same as last year at 1.25 Euros a share (a 3.3% yield), a once a year payment. Some have remarked it could have been greater, but it won’t make or break the future of the company thats for sure.

Now, the dividend is 0.90 Euros per share, or 4.17% a share

Mersen is now the leading producer of isostatic graphite in the country

What are we seeing?

Mersen has exposure to nearly every major sector out there, even ones that are deemed “ugly” by the Eurocrats; SiC, power electronics, energy production & storage, renewable energies as well as fossil fuels, fuse switches & more. All themes that are front and centre for the company however are essential to the type of power required for data centres and robotics. Currently, we’re looking at something trading sub 10X earnings when markets are in the stratosphere. I believe due to semi conductors and solar panels taking a massive hit in recent months, it has brought this company down with it. The downside that remains involves, China solar decreases, capex cycle, reduced growth & tariffs uncertainties; it could fall further certainly, but these are not existential threats to this company at all.

FY2024 they announced a two-year delay in their medium-term plan however

Closing

With record 2023 free cash flow from steady growth, record sales in 2024 and a predicted setback in growth in main sectors in 2025, a respectable P/E of <10, a decent amount of cash in the bank, and an affordable >4% dividend– the fact that this company has been falling the past year (down 37% for 1YR at time of writing) could be an interesting opportunity.

The likelihood of this company to wipe out its shareholders is rather low given their growth, secure graphite supplies, sticky clients and reasonable valuations to start; however one has to consider the economic calamities that are coming due in Europe as well as a potential contraction in demand from Chinese markets.

Interestingly, this company is not basing it’s whole business model on the Green New Scam and is geared up for the electric future of semiconductors and LEDs that run everything. It’s difficult to see that trajectory stopping even if I predict mayhem for the pensions, a major real estate crash or worse yet… In other words, I believe the company is diversified enough to withstand macroeconomic conditions.

Would I manage a whole bunch of European plays right now, just because they have fallen in recent years? No. Europe is truly in a state of collapse [of everything], but given that this company is spanning the world and all sectors, it’s an interesting diversifier play that is positioned to not only survive but perhaps thrive with nobody there to dethrone them.

What do you think?

#StayOnTheBall