Company

Lundbeck ($HLUN). It engages in the research, development, manufacturing, and commercializing pharmaceuticals for the treatment of psychiatric and neurological disorders in Europe, United States, and internationally.

Sector

Would you say that neurological and/or psychiatric disorders are going away any time soon? Absolutely not.

- Neurological + brain disorders affect ~1 billion people globally. Total cases rose from ~540M → 824M (1990 → 2021), holding the same trajectory now. Worse yet, in the United States, increases in neurological disease have increased in all type of neurological diagnosis (not one select disease).

- Depression, while being very high throughout the world impacting around 5-6% of the globe, is much higher in neurologically diseased patients: Alzheimer’s: ~60% // Parkinson’s: ~40% // Epilepsy: ~40%. Depression is one of the most common diagnosis in conjunction with other issues.

- Parkinson’s patients in the USA total around 880,000 while the global incidence growing at +1% per year

- A natural dynamic playing out is related to age-related diseases given the fact we have a rapidly aging world.

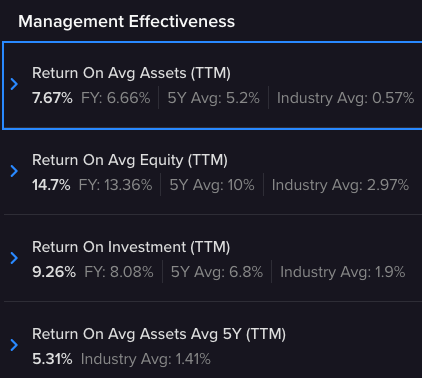

Growing Margins, Slowly but Surely

Lundbeck has transitioned away from older patent-exposed drugs toward a new core portfolio, and those drugs are growing rapidly.

Key drivers:

- Vyepti: Vyepti revenue grew ~56% YoY in 2025

- Rexulti: It’s sales grew ~28% YoY and continues expanding indications (including agitation in Alzheimer’s).

Predictable Expenses

Now their SG&A as a percentage of their sales has fallen to 37%. The point here however is the consistency that they have managed to operate during the last crazy 5 years.

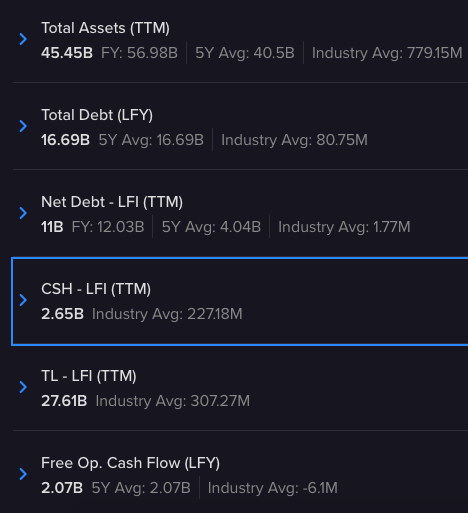

The exception to this is that they have taken a load of debt on recently which explains their high net debt increase and their financial cash flow explosion. However with the way their current assets and free cash flow sits, it doesn’t look to be troublesome for their longevity.

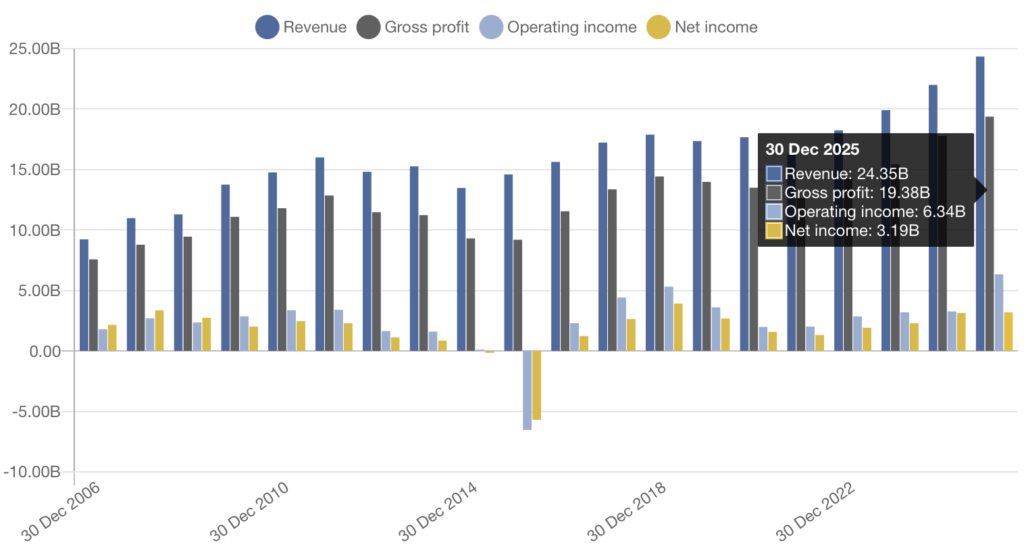

In fact, we can go back all the way to 2006 to see a relatively stable pattern between gross revenues, operating income and net income. It’s not exploding profits, but it’s reliable.

As you can see, you only have two years with negative net income in the last 20 years.

Balance Sheet

Latest Performance

(DKK)Jun 2025

Revenue 6.02B +10.45%

Net income 966M +25.45%

Diluted EPS 0.97 +24.36%

Net profit margin 16.04% +13.6%

For the fiscal year ended 31 December 2025, H Lundbeck A/S revenues increased 12% to DKR24.63B. Net income increased 2% to DKR3.19B. Revenues reflect USA segment increase of 17% to DKR13.29B, Europe segment increase of 13% to DKR5.82B, Other revenue segment increase of 6% to DKR387M.

Basic Earnings per Share excluding Extraordinary Items increased from DKR 3.17 to DKR 3.22

Share Differences Clarification

For H. Lundbeck’s $HLUN stock, Class A shares typically offer more control through voting rights, while Class B shares, often resulting from a share split, grant a smaller piece of ownership but were introduced to increase the company’s financial capacity without diluting voting rights. The specific differences for HLUN are that A-shares correspond to the original shares and have voting rights, while B-shares were created through a 4-for-1 split to increase the company’s financial resources for future growth.

For A shares:

Average volume: 91.0K

For B Shares:

Average volume: 446K

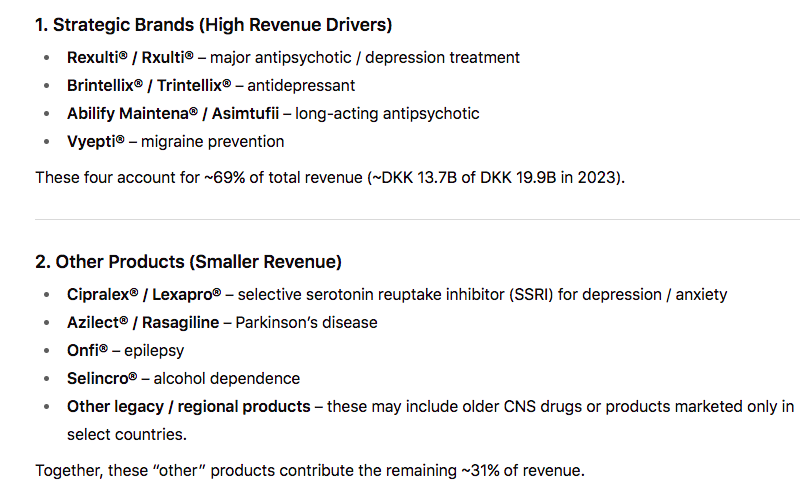

Revenue Breakdown

Growth Prospects

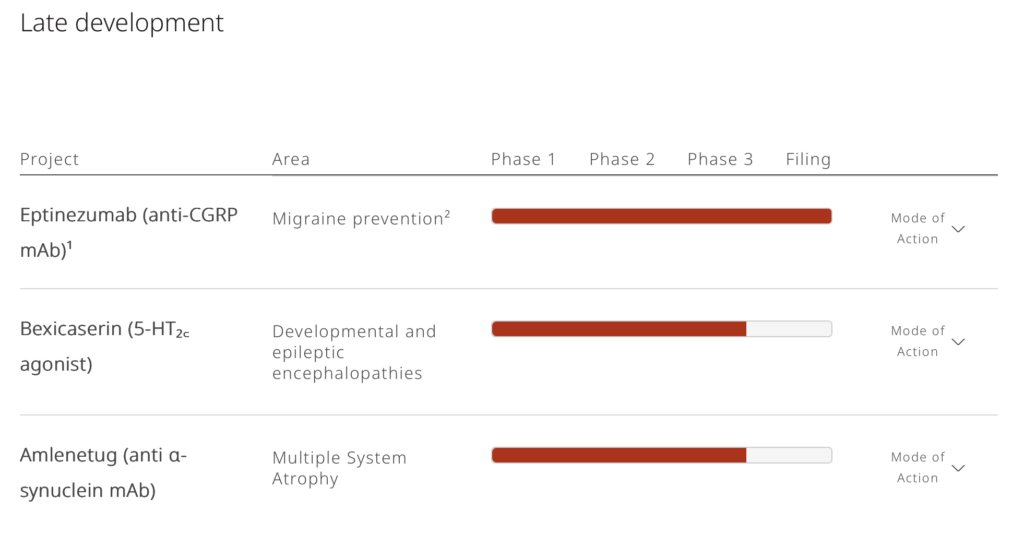

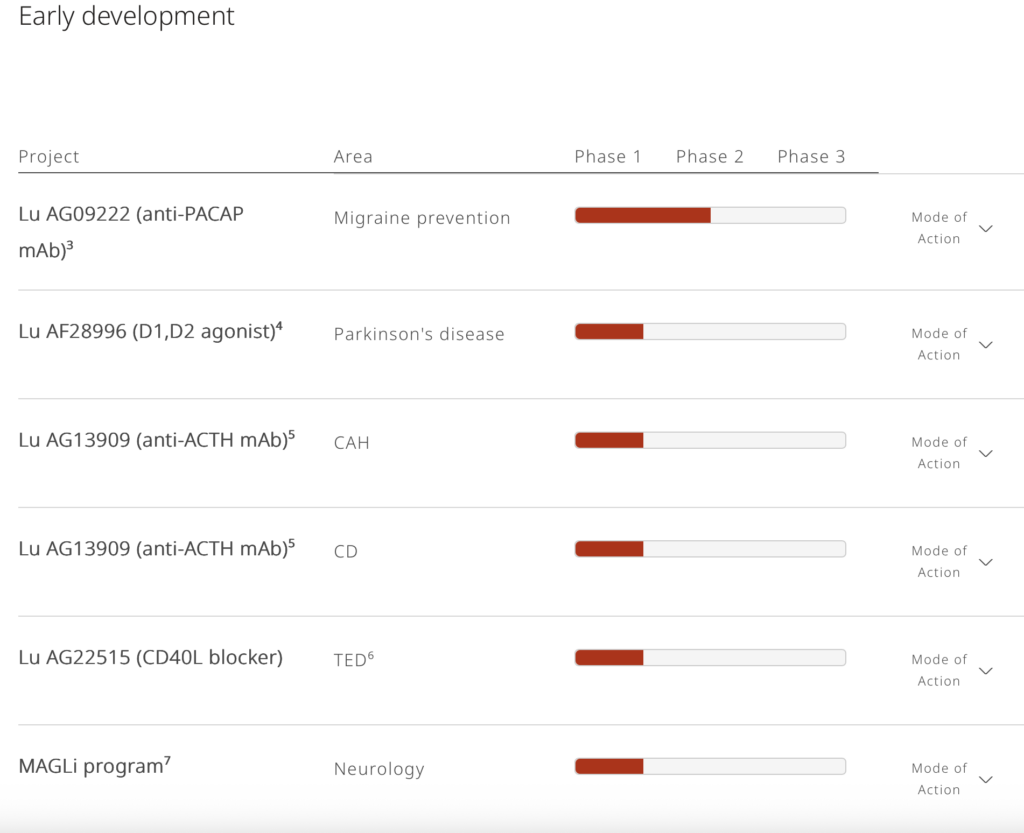

They have numerous other products in their pipeline; three are in late development while six remain in early development stages. Interestingly, Eptinezumab (anti-CGRP mAb) is now in the filing phase.

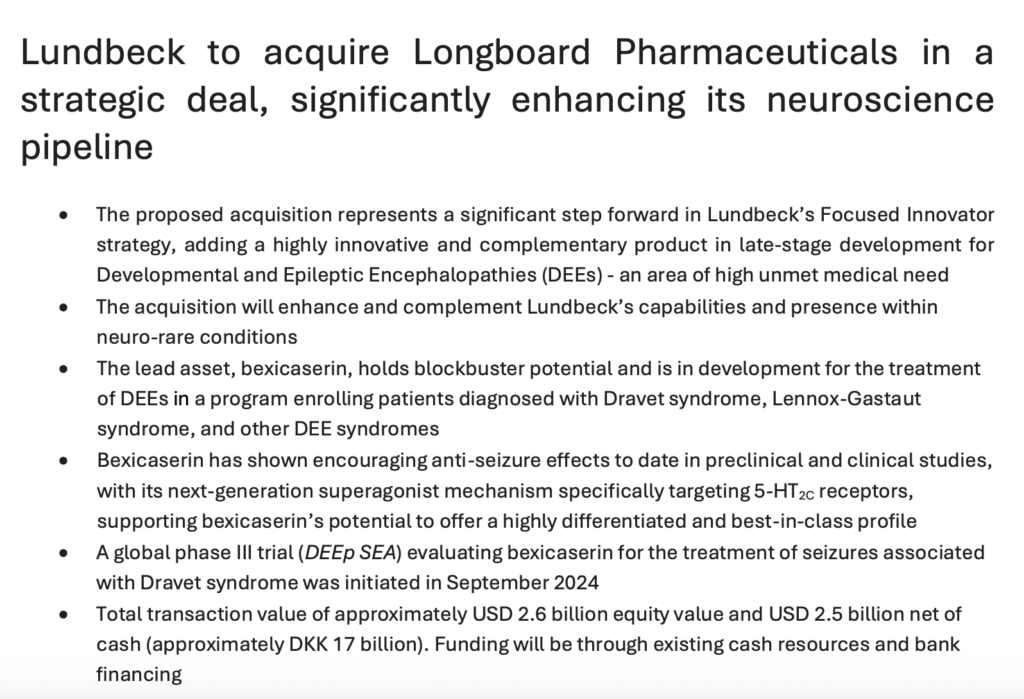

These have been made possible because of their strategic acquisition of Longboard Pharma a couple of years ago.

Are they cheap?

Market Cap

41.85B = Current

96B = Their 5YR average

We’re now seeing over a 50% fall in market cap compared to where they normally trade.

P/E ~10–12x (sometimes even <10 forward)

Meanwhile their peer pharma average closer to ~18–30x+

EV/EBITDA ~6–7x, also low… it leans towards being a quiet Pharma value stock.

Dividend

They are now supporting a payout ratio of 35%

It sits around 2.5% yield and is paid every March–reliably

Dividend per share increased from DKR0.95 to DKR1.15.

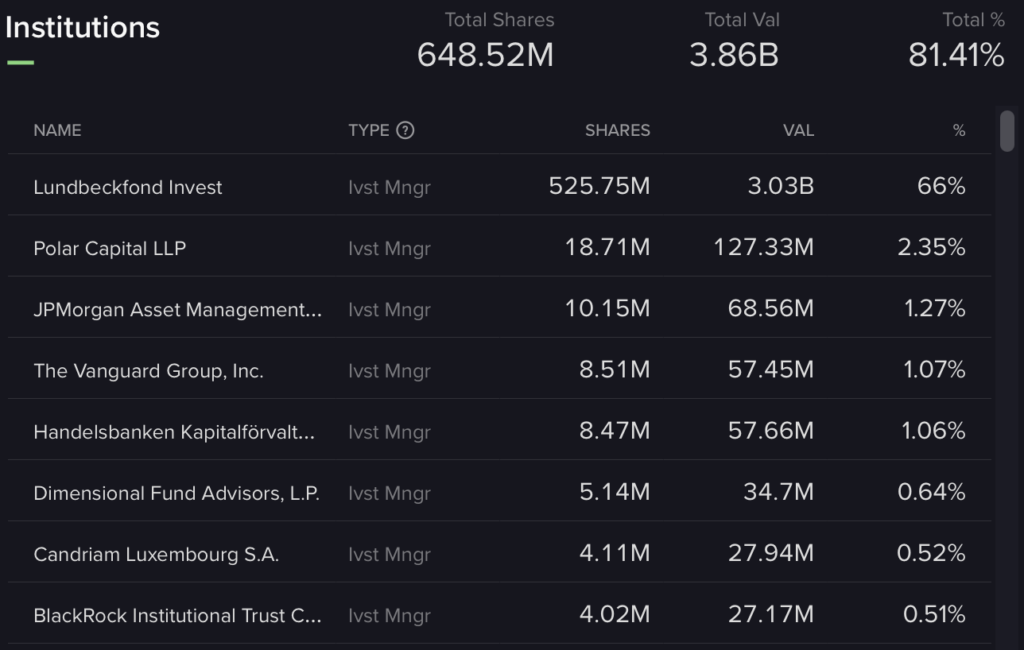

Ownership

81% of the ownership comes from institutional ownership, only 0.63% from insiders and around 18% is other (retail investors).

The Lundbeck holding company, owning a huge amount of this company greatly limits the panic sell off that could happen if markets get dicey.

Cautionary Notes

Some analysis’s suggest they have no strong “moat” in this rather broad space of drug discovery.

All of these companies also have a race against their patents too… meaning that they have to make enough money during the life of their patent OR find a new product in their pipeline that is going to offset future losses by losing their patent profits. The cost of doing business…

Summary

👍 Positives

- Cheap vs peers

- Strong positioning in CNS (specialized niche)

- Solid existing drugs with optionality in the pipeline

- Track record of stability, great valuations and earnings

⚠️ Risks

- Low growth today

- CNS drugs = high failure risk in pipeline, existing products offset this

- Patent cliffs always lurking (inherent with pharmaceuticals)

- Not a dominant “moat” company like Novo Nordisk

Closing

So, what are we looking at here? It may look pretty dull and unexciting overall. However if we look more closely, Lundbeck has been performing steadily for two decades. They’ve been keeping expenses reasonable, net incomes relatively stable and passing a plethora of products in their pipelines while paying a small dividend. They are a business that will be around longer into the future.

Notwithstanding this history and a solid balance sheet? We may ask…What’s the upside? Why own it?

Their acquisition and pipeline portfolio is the kicker. With their latest filing plus bexicaserin for rare epilepsy. This matters because it’s a rare disease causing it to go for premium price and faster adoption. The mechanism of action targets treatment-resistant epilepsy. If this receives great clinical results, it’s a potential billion dollar blockbuster–at a time, I remind you, the share price has been beaten up.

Furthermore, we’re looking at a company, despite its strong competition, unfortunately has a setup whereby the demand for its medicines is getting stronger and more global, not weaker and more concentrated.

Lastly, Vyepti, a migraine drug and Rexulti, an Alzheimer’s drug specifically for agitation (a huge unmet niche in itself) are currently scaling in their sales revenues.

Lundbeck is a company with a history of making money, trading below its peers, offering a small dividend & has expansive upside from their growing niche expertise, expanded pipeline and growing revenues with two products. Their balance sheet allows them some breathing room to express this upside for investors. It’s worth stepping back to consider this against a time when finding companies with sound fundamentals is critical, given the amounts of debts floating about.

What do you think? Are you one of the rare people who believe depression and Alzheimer’s are going away in the next 10 years?

#StayOnTheBall