Company 1

Oscar Health: Operates as a healthcare technology company in the United States

$3.65 B: Market Cap

$14.34: Share price

Cash and Investments: $3.5 Billion

Oscar Health (OSCR) recently revised its earnings guidance for 2025, highlighting expected revenue between $12 billion and $12.2 billion and operational losses of $200 million to $300 million. This revision coincided with the company’s shares gaining 22% over the last quarter, amidst a backdrop of increased optimism in the broader markets exemplified by the S&P 500 reaching record highs.

EPS: 0.48

Debt/Equity Ratio: 22.4%

CEO Mark Bertolini’s $11.92 million insider share purchase signals strong internal conviction in Oscar’s turnaround plan

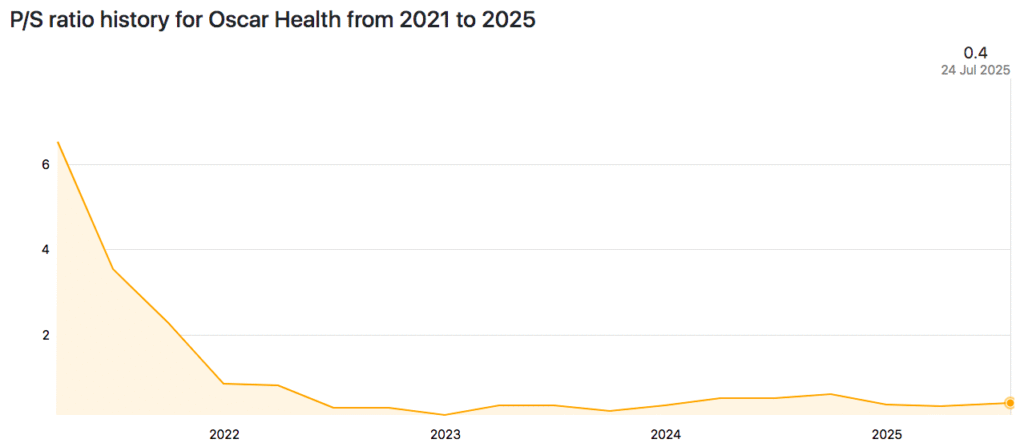

The Ratio that stood out

I have seen others noting that the P/S was as low as 0.3 (depending on the trading day). Is this coming from a drop in share price? No. It’s their sales are growing higher and higher:

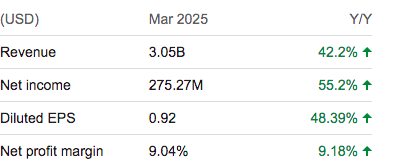

According to Oscar Health‘s latest financial reports the company’s current revenue (TTM) is $10.08 Billion USD. In 2024 the company made a revenue of $9.17 Billion USD an increase over the revenue in the year 2023 that were of $5.86 Billion USD.

Earnings in 2025 (TTM): $0.16 Billion USD

In 2024 the company made an earning of $57.16 Million USD, an increase over its 2023 earnings that were of -$0.25 Billion USD

Company 2

Wrap Technologies, Inc. (NASDAQ: WRAP) is a Miami, Florida-based global leader in public safety technology and services, founded in 2016, that develops innovative non-lethal policing solutions for law enforcement and security personnel across the Americas, Europe, the Middle East, Africa, and the Asia Pacific. The company’s flagship product, the BolaWrap® 150, is a handheld remote restraint device that discharges a seven-and-a-half-foot Kevlar tether to safely entangle individuals from a distance of 10–25 feet, complemented by a broader portfolio that includes Wrap Reality VR training platforms, WrapTactics™ training programs, and Wrap Intrensic body-worn camera and digital evidence management solutions.

In 2025, Wrap reported full-year gross revenue of $5.2 million, representing 15% year-over-year growth, while also launching Wrap Federal, a wholly owned subsidiary targeting U.S. Department of Defense and Department of Homeland Security contracts focused on non-lethal and counter-UAS solutions

Wrap technologies is another great growth play that is relatively underplayed (even though its product received widespread acknowledgement for being “Batman-like”).

Management recently raised $5 million and stated the company is not actively seeking additional capital at this time.

Wrap Technologies posted a 62% revenue surge in the last year. Their gross margins expanding 500 basis points to 52% and operating losses narrowing 15%.

WRAP just signed a deal with a large UK defense contractor for anti-drone devices called the Merlin-1 line of product, too.

At the time of writing they hold $1.05 million of net cash.

- Stock price: ≈ $1.43 – $1.62

- Market cap: ≈ $79M – $80M

🧾 Balance sheet

- Total assets: ≈ $15M – $18M (recent quarters)

- Total liabilities: ≈ $2M – $4M

📉 Earnings

- EPS (TTM): ≈ –$0.14 to –$0.20

I’ve been aware of this technology for a little while–but it wasn’t until a subscriber on State Speculator pointed out this company as being a beneficiary of internal US chaos (please read that article below)

https://statespeculator.substack.com/p/stability-isnt-free-what-happens

Company 3

$IFRX InflaRx N.V.

A clinical-stage biopharmaceutical company, discovers and develops inhibitors using C5a technology in Germany and the United States. They are focused on discovering and developing highly potent inhibitors targeting the complement activation factor C5a and its receptor C5aR to treat severe autoimmune and inflammatory diseases–this is a novel space utilizing vilobelimab (GOHIBIC), a first-in-class anti-C5a monoclonal antibody.

Latest research indicates not only it’s ability to put skin ulcers into signs of remission but it has also recently been showing clinically relevant reduction in drug-drug interactions and liver toxicity.

Not only this, but they’re demonstrating 70% growth guidance for this year with very little debt/short term liabilities.

However, this is a pre-revenue play, burning free cash flow conditional upon clinical results, certifications and whether their pipeline can become commercially viable.

Stock price: ≈ $1.62 – $1.66

Market cap: ≈ $115M – $117M

Balance sheet

- Total assets: ≈ $64.9M

- Total liabilities: ≈ $16.0M

(Other sources show similar ranges depending on currency conversion and reporting period — roughly $55M–$65M assets and ~$13M–$16M liabilities.)

Earnings

EPS (TTM): ≈ –$0.68 to –$0.80

Different Approach

Normally I am geared towards writing about resource companies or some sort of boring, but stable long-term play. These companies fit a different category–it is purely a growth play whereby this company growth in sales is increasing more and more but it’s shares haven’t demonstrated this added revenue boost or contractual agreements.

Investment Manager

Managed Accounts. If you like the way On The Ball considers investment opportunities and you’d like a tailored professional service yourself. Please contact