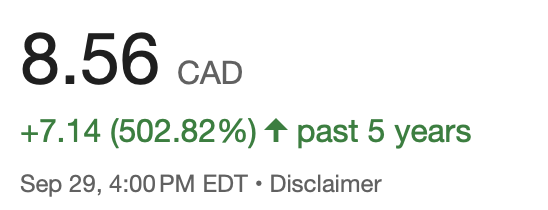

Disclaimer: When I started writing about this stock, the share price exploded. I’m glad our thesis is correct but the immediate upside is now far more limited. Quick Share!

Company

Andean Precious Metals Corp. is a Canada-based precious metals producer. The Company is focused on expanding into top-tier jurisdictions in the Americas. It is engaged in the exploration, exploitation, treatment, refining and commercialization of dore containing silver and gold, which it extracts from its own mining rights and through purchased third-party material. The Company’s segments include Bolivia and United States of America. The Company owns a 100% interest in, through direct and indirect interests, Empresa Minera Manquiri S.A. (Manquiri) which is the operator of the San Bartolome processing facility, near Potosi, Bolivia. It also holds interest in Golden Queen Mining LLC, which is situated in Kern County, Southern California on 1,100 hectares

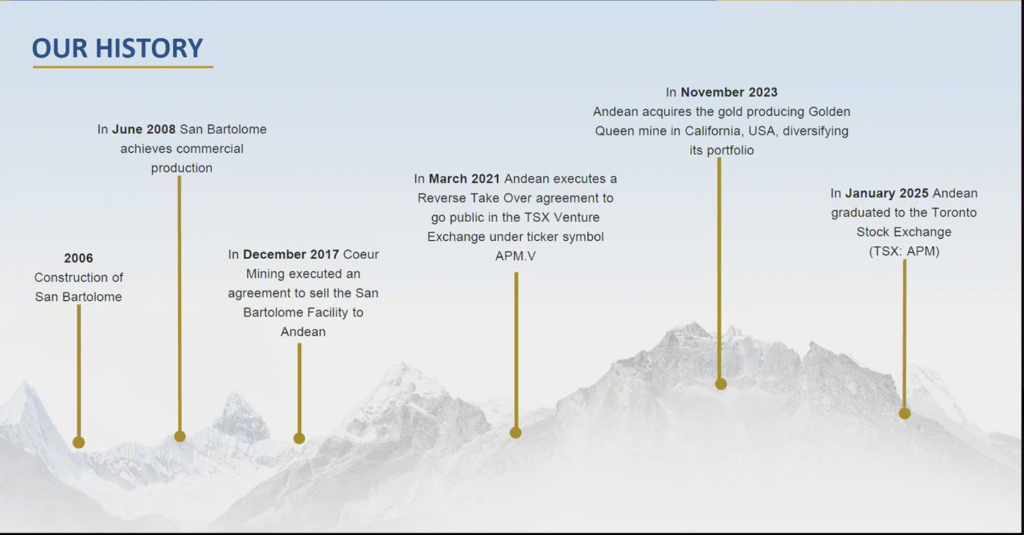

They had an interesting method on how they decided to get going… if you see in 2017, when they bought the San Bartolome mine, it only had 1 year Life of Mine remaining. Rather than try to squeeze it out for 365 days, they tried to maximize the facility by buying ore from other producers to operate as a processing plant before they could acquire their own producing assets (something they continue to do today)

Ratios

P/E: 16.12

P/B: 0.93

P/S: 0.59

Update

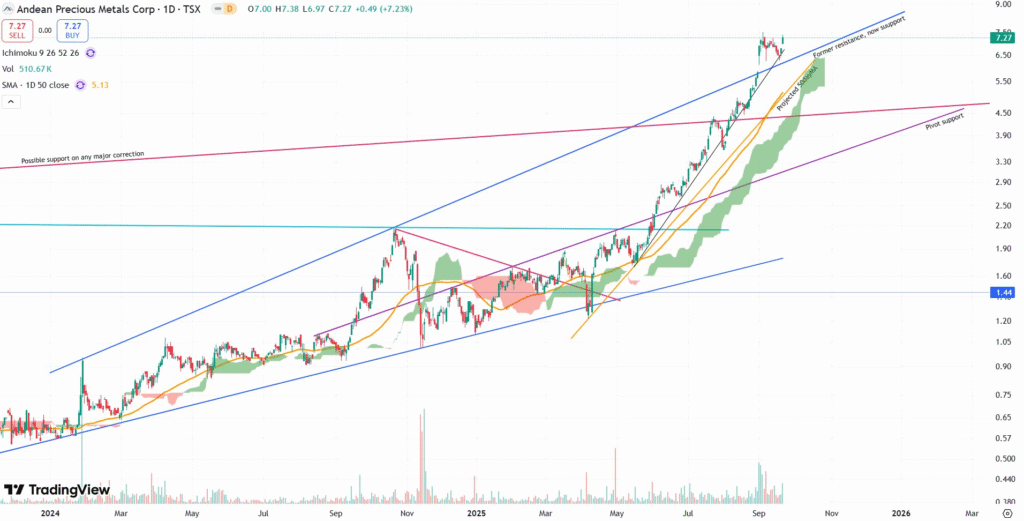

The share price and valuations are getting ahead of it.

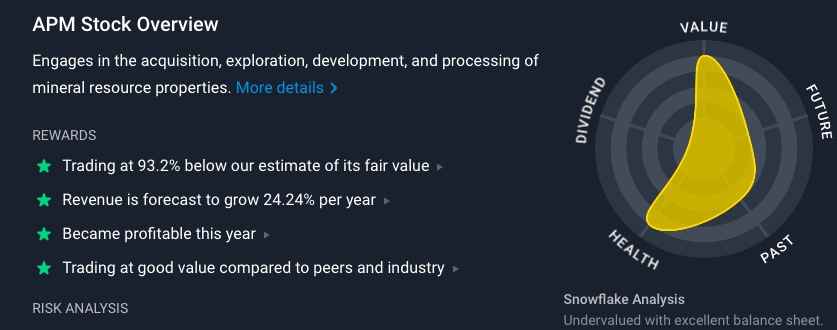

Simply Wall St thinks highly of it

Projects

The company has projects in California and in Bolivia; half and half with gold and silver.

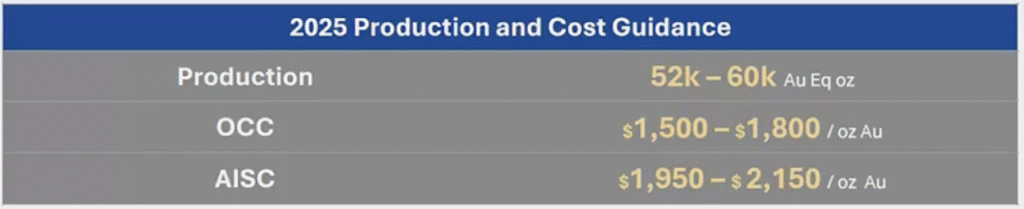

Golden Queen is currently being examined to extend their mine life through further exploration, paying for itself. They are permitted in the commercialization of turning their waste into aggregates even after the gold mine is finished (though I don’t think this adds much to the investment case). Its currently producing 60k oz forward run rate with $2100 AISC and the AISC also includes G&A spending.

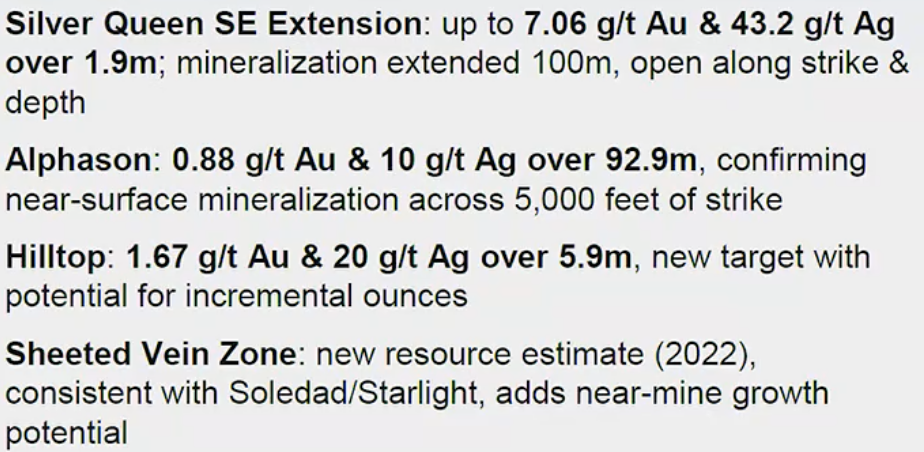

Here are some of their exploration results they’ve hit so far to state a case of extending the life of mine.

| Asset | Reported Life of Mine / Life of Operations |

|---|---|

| San Bartolomé (Bolivia) | ~ 4.6 years based on the updated 2P mineral reserves. |

| Golden Queen / Soledad Mountain (USA) | 5 years |

Interestingly, their Bolivian asset also has a probable ~11.95 million ounces of silver (at ~93 g/t crazy high grade) in their latest resource estimate–so it’s like that LOM can be extended as well.

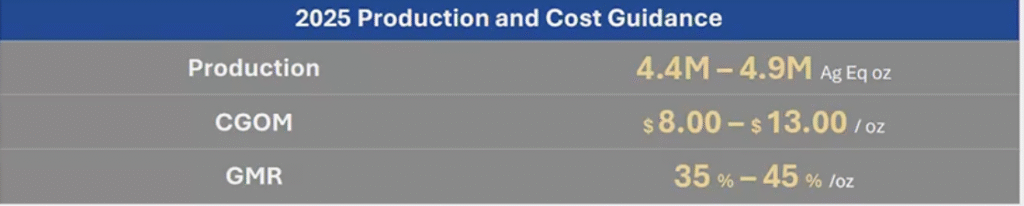

You can see the margins here are fantastic too. Their facility can process 1.8 million tonnes per year. It’s worth noting however that they’re subject to a 7% royalty and a high tax rate of 32% however. Currently, Bolivia that will be producing upwards of 200mil USD FCF/yr in 2027 onwards. Currently producing about 80mil FCF.

The good part however is that they’re able to process silver and other minerals from other companies nearby or their own projects which is made possible with these higher grades.

Cash

31 March 2024, Andean Precious Metals Corp revenues increased 87% to $43.1M. Net loss totaled $76K vs. income of $219K. Revenues reflect an increase in demand for gold and copper during this ongoing bull market.

They also have a $36M credit facility available to them.

Things I like

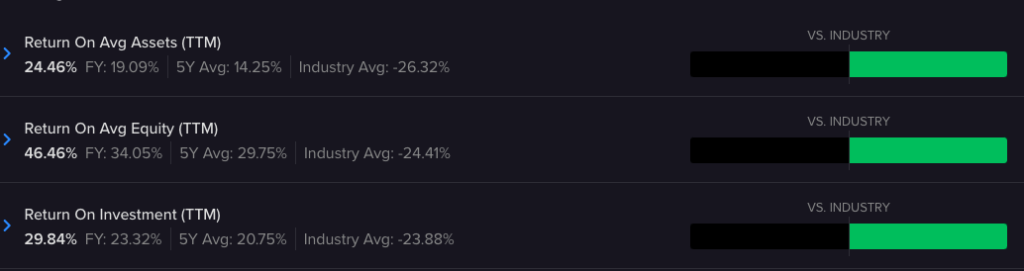

- The company just came into profits and is trading at a very good valuation for a mining company

- The returns are quite good and they are leveraged to the underlying price of the rising commodity markets. Their plant in Bolivia stands to gain from others in the region mining.

- Very high grade with an ample resource; bypass Mexican mining risk by being in Bolivia + Tier-1 mining jurisdiction with USA

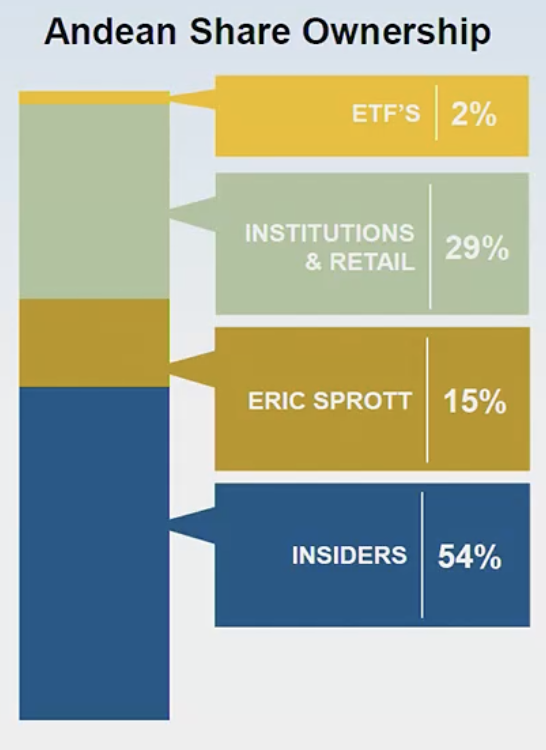

- Tight ownership but ETF exposure coming

- Obviously commodity prices at highs for them

- Still at least 4 more years of high margin runway assuming they don’t explore deposits further

Things to Watch

- News regarding their life of mines

- Bolivia (is really falling apart and incredibly unstable) + California is one of the least business friendly states

- Whether share price starts to become unreasonable and there are simply better options out there

Closing

This is a shorter post because I feel slightly bad that the stock has already performed so well and that there is little of a “case” I can state for it for you to get in early and realize the results. Speaking of that however, I encourage you to join as a member to do just that–get results.

It also helps we discuss other big picture stocks outside of stock equities and hold a consultancy service that you are free to use with discounts at any time!

Either way, I still feel like there is upside with Andean and I wanted to publish it regardless. If we look at gold and silver equities they have exploded recently, but still, when we compare them to the rest of the inflated market, the supply constraints ahead and the fact that virtually no funds are allocated to precious metals (yet), the opportunities are still immense for not only preservation but capital growth. I believe it will be the growth we need if we want to survive the storm ahead.

I look forward to chatting with you as an On The Ball member!